Remote KYC is the process of verifying a customer’s identity through digital channels without requiring an in-person meeting. It powers modern remote identity verification across banking, fintech, payments, crypto, insurance and other online services. Businesses rely on remote onboarding KYC to deliver fast, secure and scalable access to financial products.

Online KYC verification can reduce onboarding time and expand access for customers worldwide, but it also introduces serious risks. Fraudsters exploit forged documents, impersonation, synthetic identities, deepfakes and stolen personal data to bypass weak controls. According to Juniper Research, global losses from online payment fraud are expected to exceed $343 billion between 2023 and 2027, highlighting the need for stronger remote identity verification systems.

This guide explains how remote KYC works, the technologies behind digital identity verification, and the compliance expectations businesses must meet. It also covers common fraud risks and the controls required to build a secure and reliable remote onboarding KYC process that protects both businesses and customers.

Binderr Remote KYC Software

Choosing the right remote KYC solution is critical for balancing speed, security, and compliance.

- AI-powered KYC identity verification with document checks and OCR extraction

- Biometric face matching and liveness detection to prevent spoofing

- AML screening across sanctions, PEPs, watchlists, and adverse media

- Dynamic risk scoring for automated decision-making

- UBO identification and ownership structure mapping

- Custom onboarding workflows, forms, and e-signatures

What Is Remote KYC?

Remote KYC is a digital process that verifies customer identity and assesses risk without in-person meetings. It uses tools like document uploads, OCR, facial recognition, liveness checks, and database verification, along with AML screening (sanctions, PEPs, adverse media) and risk scoring. Unlike basic identity checks, it also evaluates customer risk and compliance with financial crime regulations, forming the foundation of remote identity verification and remote onboarding KYC workflows.

Run Your First KYC Check

Why Is Remote Identity Verification Important?

Unlock seamless digital onboarding while strengthening security with remote identity verification and remote onboarding KYC.

Discover how online KYC, biometric verification, and fraud prevention tools are transforming customer trust and compliance.

Faster Customer Onboarding - Automated document verification, biometric checks and database validation can significantly speed up remote KYC by removing the need for in-person appointments and manual reviews. Customers can submit identity documents and complete verification in minutes, allowing businesses to approve accounts faster while maintaining compliance in remote onboarding KYC environments.

Wider Customer Access - Remote identity verification enables customers to complete KYC from anywhere in the world using a smartphone or computer. This flexibility supports global onboarding, allowing businesses to reach users across different countries, regions and time zones without requiring physical presence.

Lower Operational Workloads - Automation in digital KYC reduces the burden of repetitive tasks such as data entry, document comparison and initial screening. By handling these processes automatically, compliance teams can focus on higher-risk cases and more complex customer due diligence activities within remote onboarding KYC systems.

More Consistent Verification - Standardised workflows and predefined verification rules help ensure that every customer is assessed using the same criteria. This reduces inconsistencies between reviewers and improves the reliability of remote identity verification decisions across the onboarding process.

Stronger Fraud Detection - Remote KYC systems combine document analysis, biometric face matching, liveness detection and device intelligence to identify potential fraud. These layered controls provide stronger protection against identity theft, deepfakes and synthetic identities compared to relying on simple document copies.

Improved Customer Experience - A well-designed remote onboarding KYC process improves customer experience by offering clear instructions, mobile-friendly interfaces and quick feedback. Minimising unnecessary document requests and reducing friction helps customers complete identity verification smoothly and efficiently.

Start KYC Verification for Free

Discover the Journey Behind Seamless Remote KYC Verification

Explore how remote KYC, remote identity verification, and remote onboarding KYC workflows combine digital identity verification, biometric checks, and automated compliance processes to create secure and efficient customer onboarding experiences.

Step 1: Customer Information Collection

The remote KYC process begins with collecting essential customer information to establish a baseline identity profile. This stage is critical for remote identity verification and ensures that businesses gather accurate data for compliance and risk assessment. Typical details include:

- Full legal name: The person’s official name as shown on legal documents.

- Date of birth: The exact birth date used to confirm age and identity.

- Nationality: The country or countries the person is legally a citizen of.

- Residential address: The current home address where the person lives.

- Contact details: Phone number and email used for communication.

- Tax residency: The country where the person is liable to pay taxes.

- Occupation or business activity: The person’s job or main source of income.

- Intended account or service use: The purpose for opening the account or using the service.

Businesses should clearly explain how this personal data will be used, stored, and protected in line with data protection regulations. Obtaining explicit consent is essential, particularly when processing sensitive information as part of remote onboarding KYC and AML compliance.

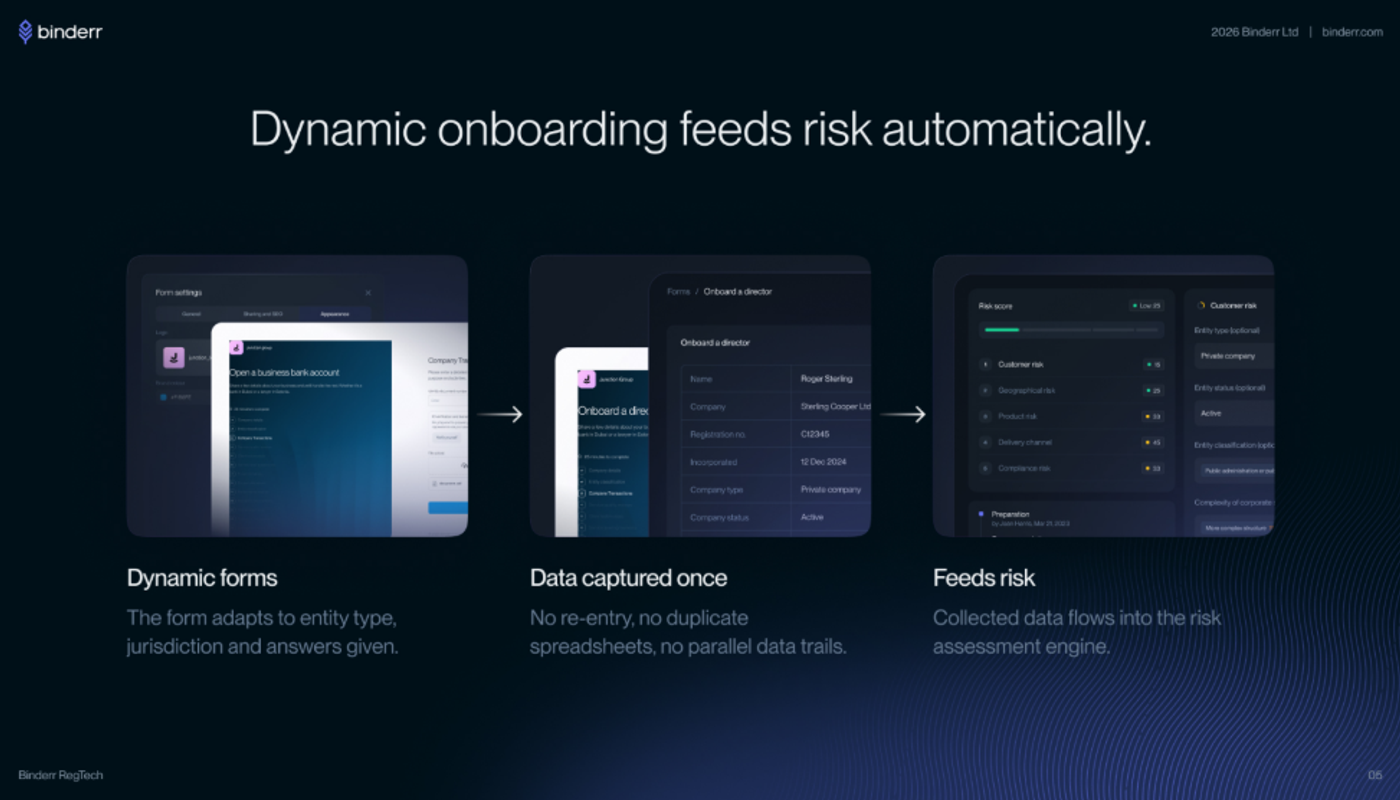

Binderr connects onboarding data with risk

Binderr Compliance uses dynamic onboarding forms that can adapt according to the customer, jurisdiction and answers provided. Information is captured once and passed directly into the risk assessment process, reducing duplicate data entry and disconnected compliance records.

(Binderr connects dynamic onboarding forms with automated customer risk assessment.)

Step 2: Identity Document Capture

Once customer details are collected, the next step in remote identity verification is capturing a valid identity document. Customers are typically asked to upload or photograph an accepted document, such as:

- Passport: A government-issued document used for international travel and identity verification.

- National identity card: An official ID issued by a country to confirm a person’s identity and citizenship.

- Driving licence: A permit that allows a person to drive and also serves as a form of identification.

- Residence permit: A document that proves a person’s legal right to live in a country.

To improve accuracy and reduce verification errors, digital onboarding platforms should provide real-time guidance. This includes prompts to avoid glare, ensure proper lighting, prevent blur, and capture the full document within the frame. High-quality document capture is essential for reliable automated KYC verification.

Step 3: Document Data Extraction

After the document is captured, Optical Character Recognition (OCR) technology is used to extract key data fields. This automation reduces manual input errors and speeds up the digital KYC process. Extracted information may include:

- Document number: A unique identifier assigned to the identity document.

- Full name: The person’s legal name as shown on the document.

- Date of birth: The individual’s birth date used to confirm age and identity.

- Expiry date: The date after which the document is no longer valid.

- Issuing country: The country that issued the identity document.

- Machine-readable zone (MRZ) data: Encoded text on the document used for automated verification.

- Address, where available: The residential address listed on the document, if included.

The system then cross-checks this extracted data against the information provided by the customer. Any inconsistencies may trigger additional verification steps or manual review, helping strengthen fraud prevention in remote customer onboarding.

Step 4: Document Authenticity Checks

To ensure the document is genuine, the system performs a series of authenticity checks. These checks are crucial in detecting forged or tampered identity documents during online identity verification. The system may analyse:

- Document templates: Check if the document matches official formats used by issuing authorities.

- Security features: Verify built-in protections like watermarks, microtext, and UV elements.

- Fonts and spacing: Ensure text style and alignment are consistent with genuine documents.

- Holograms: Confirm presence and correct appearance of holographic elements.

- Machine-readable zones: Validate encoded data for accuracy and proper structure.

- Barcodes: Scan and compare barcode data with visible document details.

- Photograph placement: Check if the photo is correctly positioned and not tampered with.

- Signs of digital alteration: Look for edits, overlays, or inconsistencies in the image.

- Expiry and issue dates: Confirm dates are valid and logically consistent.

- Lost or stolen document databases, where available: Cross-check against records of reported documents.

These layered checks help identify inconsistencies and reduce the risk of identity fraud, making automated KYC verification more robust and reliable.

Step 5: NFC Chip Verification

Some modern identity documents, such as electronic passports and national ID cards, contain embedded NFC (Near Field Communication) chips. During remote KYC, compatible devices can read this chip to access securely stored identity data.

The system compares the chip data with the visual document and validates cryptographically signed information, providing a higher level of assurance. While NFC verification strengthens digital identity verification, it is not universally available due to device limitations and document compatibility, so it is typically used as an additional verification layer rather than a standalone solution.

Step 6: Selfie and Facial Comparison

In this stage of remote KYC and digital identity verification, the customer captures a selfie or short video using their device. Advanced facial recognition technology then compares this live biometric image with the photograph on the submitted identity document. This process helps confirm that the person presenting the document is the rightful owner, reducing the risk of impersonation and identity fraud during online KYC verification.

There are two key approaches to biometric matching. One-to-one face verification compares the customer’s selfie directly with the image on their identity document to confirm a match. One-to-many biometric identification, by contrast, compares the face against a broader database to identify the individual. Remote KYC processes typically rely on one-to-one verification because it is faster, more privacy-conscious, and aligned with standard digital customer onboarding requirements.

Step 7: Liveness and Deepfake Detection

Liveness detection is a critical layer in remote identity verification that ensures the biometric input comes from a real, physically present person rather than a spoofed source. It helps prevent fraud attempts involving printed photos, screen replays, masks, pre-recorded videos, face-swapping tools, or AI-generated deepfake media. Without liveness checks, even accurate facial recognition systems can be vulnerable to presentation attacks.

There are two main types of liveness detection used in online identity verification. Active liveness requires the customer to perform a prompted action, such as blinking, smiling, or turning their head. Passive liveness, on the other hand, evaluates subtle cues like texture, lighting, and motion without requiring user interaction. Combining both methods strengthens fraud prevention and improves the reliability of biometric KYC verification.

Step 8: Contact, Address, and Database Verification

As part of the remote KYC process, businesses may verify additional customer details depending on the level of risk and regulatory requirements. This can include confirming mobile phone ownership through OTP verification, validating email addresses, checking residential addresses, and cross-referencing government or credit bureau databases. Trusted digital identity credentials may also be used to support identity proofing.

It is important to note that database checks should complement, not replace, primary identity verification methods such as document verification and biometric matching. While databases can provide useful corroborating evidence, relying solely on them may introduce inaccuracies or outdated information. A layered approach ensures stronger digital identity verification and more reliable customer onboarding outcomes.

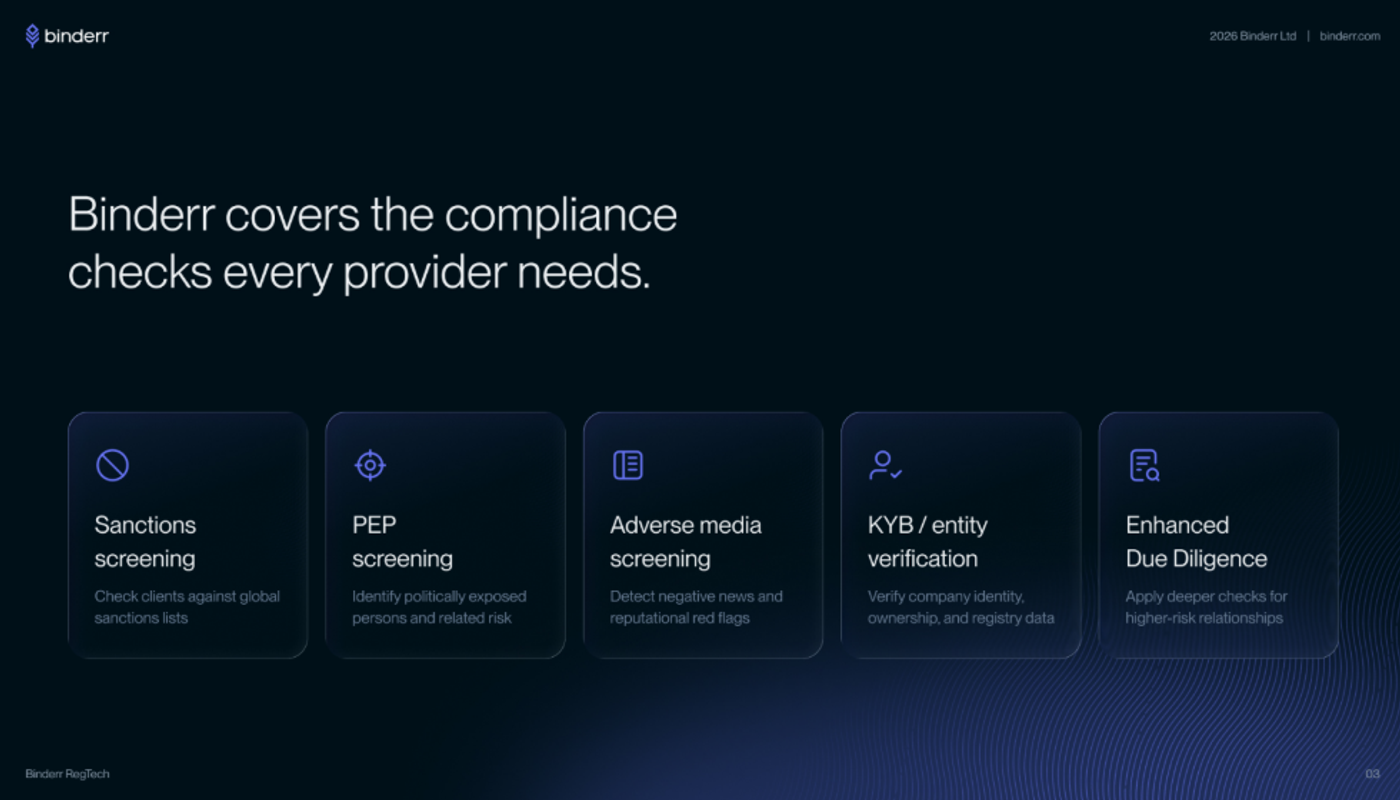

Step 9: AML and Financial Crime Screening

Once identity verification is complete, the customer must be screened against various financial crime databases as part of AML compliance. This includes checks against sanctions lists, politically exposed person (PEP) databases, global watchlists, adverse media sources, internal blocklists, and known fraud records. These checks help identify individuals who may pose regulatory, reputational, or financial risks.

While identity verification confirms that a person is who they claim to be, AML screening evaluates whether that verified identity is associated with financial crime risks. This distinction is essential in remote KYC workflows, as a legitimate identity can still present compliance concerns. Integrating AML screening into digital onboarding ensures that businesses meet regulatory obligations and reduce exposure to illicit activity.

Screen verified customers for wider compliance risks

Remote identity verification confirms who a customer is, but screening helps determine the risk associated with that identity. Binderr Compliance brings sanctions screening, PEP checks, adverse media analysis and enhanced due diligence into a connected workflow, allowing compliance teams to move from identity verification to risk assessment without switching between separate systems.

(Binderr Compliance combines sanctions, PEP and adverse media screening with enhanced due diligence workflows.)

Try FREE AI-powered AML screening with Binderr

Step 10: Customer Risk Scoring

Customer risk scoring is a key component of automated KYC verification, enabling businesses to assess the overall risk profile of each applicant. Risk models typically consider multiple factors, including customer location, nationality, product type, occupation, and intended transaction activity. Additional inputs such as PEP status, sanctions exposure, adverse media findings, and source of funds concerns further refine the risk assessment.

Technical signals also play a role in digital identity verification risk scoring. These may include device anomalies, document authenticity indicators, and biometric verification confidence levels. By combining these data points, businesses can assign a risk score that determines whether a customer qualifies for standard onboarding, requires enhanced due diligence, or should be rejected.

Step 11: Automated Decision or Manual Review

After completing identity verification, AML screening, and risk scoring, the system generates an onboarding decision. Possible outcomes include approval, rejection, requests for additional information, referral for manual compliance review, or escalation to enhanced due diligence. Automated KYC systems can process low-risk cases quickly, improving efficiency and customer experience.

However, businesses should avoid automatically rejecting customers based on a single technical failure, such as a poor-quality image or temporary biometric mismatch. Instead, uncertain or borderline cases should be routed to manual review, where trained compliance teams can assess the situation more accurately. This balanced approach helps reduce false rejections while maintaining strong fraud prevention and regulatory compliance.

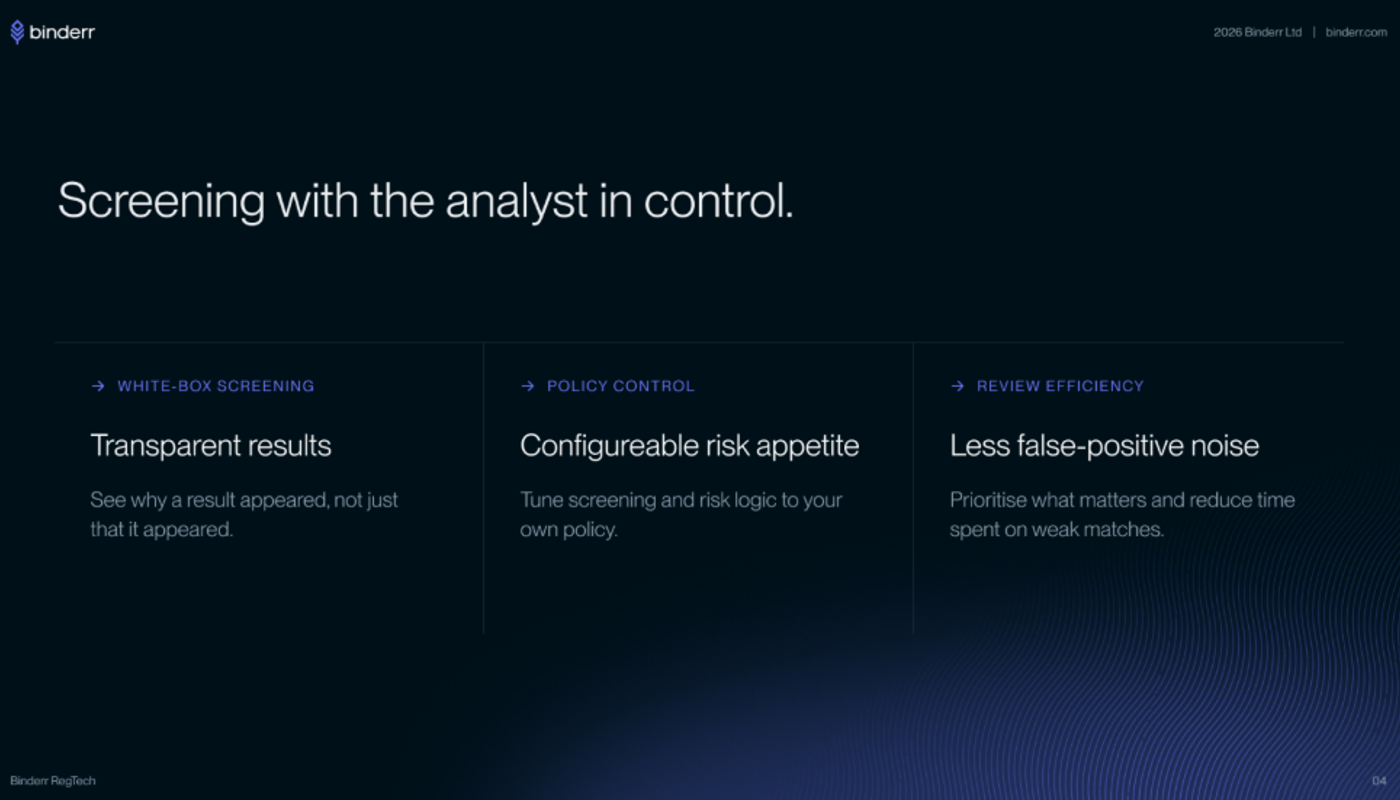

Automated screening should help analysts make better decisions rather than produce unexplained pass-or-fail outcomes. Compliance teams need to understand why a match appeared, apply their own screening policies and prioritise results that require genuine investigation.

Binderr keeps analysts in control by showing the reasons behind screening results and allowing teams to configure screening logic around their own risk appetite. This helps reviewers distinguish meaningful matches from weaker alerts and document why a customer was approved, rejected or escalated.

See How Binderr Streamlines Remote KYC

Binderr simplifies the entire remote onboarding process by combining multiple compliance checks into one workflow:

- Run KYC, KYB, and AML checks simultaneously

- Automatically extract and verify identity data

- Perform biometric verification and liveness detection

- Screen customers against global risk databases

- Assign dynamic risk scores instantly

- Route cases to manual review when needed

Remote KYC vs Identity Verification

Discover how remote KYC and identity verification work together to build secure, compliant digital onboarding experiences.

Understand the key differences between identity verification, customer due diligence, and AML screening in modern remote KYC processes.

Identity Verification | KYC |

Confirms that a claimed identity is genuine | Evaluates the customer and their wider compliance risk |

Checks documents and biometric information | Includes identity checks, AML screening and risk assessment |

Usually concentrated at onboarding | Continues throughout the customer relationship |

Focuses on impersonation and identity fraud | Focuses on identity, money laundering, sanctions and customer risk |

Produces a verification result | Produces an onboarding and risk decision |

Try Advanced Identity Verification Features for Remote KYC with Binderr

Binderr’s key capabilities include:

- AI-powered document verification across 230+ countries

- Support for 11,000+ ID types globally

- OCR data extraction for instant processing

- Biometric face matching with high accuracy

- Liveness detection to prevent spoofing

- Multi-layered fraud signals for risk analysis

Is Remote KYC Compliant?

Remote KYC can be compliant when it combines reliable identity checks, a risk-based approach, and adherence to AML, KYC, and data protection regulations. Remote identity verification and remote onboarding KYC processes must align with jurisdiction-specific requirements while maintaining strong identity assurance and fraud prevention controls.

FATF Digital Identity Guidance

The Financial Action Task Force (FATF) provides global guidance on how digital identity systems can support customer due diligence (CDD) and remote KYC. FATF does not mandate specific technologies but instead outlines principles that ensure trust and reliability in remote identity verification systems.

Key principles include:

- Understanding the digital identity system’s assurance level, including how identity proofing and authentication are performed.

- Evaluating the underlying technology, architecture, and governance of the identity verification solution.

- Determining whether the system is sufficiently reliable, independent, and resistant to fraud.

- Matching the level of identity verification to the risk profile of the customer, product, and transaction.

- Maintaining full responsibility for customer due diligence decisions, even when using third-party KYC providers.

FATF supports the use of remote identity verification and remote onboarding KYC processes for AML compliance, provided that organisations assess their effectiveness and suitability. Businesses cannot rely blindly on automated tools—they must understand how those tools operate and whether they meet regulatory expectations for identity assurance and fraud prevention.

European Banking Authority Guidelines

The European Banking Authority (EBA) has introduced detailed guidelines for remote onboarding KYC, particularly for EU-based credit institutions, fintech companies, and financial service providers. These guidelines emphasise a risk-based approach and require firms to demonstrate that their remote KYC processes are secure, reliable, and auditable.

Key expectations include:

- Establishing clear remote onboarding policies and procedures.

- Conducting due diligence on identity verification tools and third-party providers.

- Ensuring the reliability and accuracy of document verification and biometric checks.

- Performing accurate customer matching through biometric identity verification.

- Managing ICT and cybersecurity risks associated with digital onboarding platforms.

- Implementing quality control measures, including manual review processes.

- Conducting ongoing monitoring of customer activity and risk profiles.

The EBA guidelines are technology-neutral, focusing on outcomes rather than specific tools. Businesses must demonstrate that their remote KYC and remote identity verification processes effectively mitigate fraud risks, support AML compliance, and provide a reliable audit trail.

NIST Digital Identity Guidelines

The National Institute of Standards and Technology (NIST) provides a widely recognised framework for digital identity verification, particularly in the United States. The updated NIST SP 800-63-4 guidelines divide digital identity into three core components: identity proofing, authentication, and federation.

These guidelines introduce several important concepts:

- Identity Assurance Levels (IAL): Measure the confidence that a claimed identity is genuine.

- Authenticator Assurance Levels (AAL): Define the strength of authentication methods used to access systems.

- Federation Assurance Levels (FAL): Address how identity information is shared between systems and organisations.

- Risk-based selection of assurance levels depending on the sensitivity of the service or transaction.

- Consideration of privacy, security, and usability when designing identity verification systems.

While NIST guidelines are primarily designed for US federal systems, they are widely adopted by organisations building secure remote KYC and remote identity verification solutions. They provide a structured approach to balancing security, user experience, and compliance in remote onboarding KYC environments.

UK Digital Identity Requirements

In the United Kingdom, updated guidance clarifies how certified digital identity services can be used within the framework of the Money Laundering Regulations. These rules allow businesses to rely on approved providers for remote identity verification, provided certain conditions are met.

However, using a certified provider does not transfer regulatory responsibility. Businesses must still:

- Assess the overall risk profile of each customer.

- Complete all required customer due diligence (CDD) checks.

- Apply enhanced due diligence (EDD) for higher-risk customers.

- Maintain accurate records and audit trails.

- Ensure that the chosen identity verification provider is appropriate and reliable.

This means that remote onboarding KYC must be part of a broader compliance framework. Remote identity verification alone does not satisfy all AML obligations—it must be combined with risk assessment, screening, and ongoing monitoring.

Privacy and Biometric Data Requirements

Remote KYC and remote identity verification involve processing highly sensitive personal data, including identity documents and biometric identifiers such as facial images. As a result, businesses must comply with strict data protection and privacy regulations, such as GDPR and similar frameworks worldwide.

Key considerations include:

- Establishing a lawful basis for processing personal and biometric data.

- Recognising that biometric data is often classified as special-category data requiring additional safeguards.

- Applying data minimisation principles to collect only necessary information.

- Defining clear data retention limits and deletion policies.

- Using encryption to protect data in transit and at rest.

- Implementing strong access controls and authentication mechanisms.

- Providing transparent privacy notices explaining how data is used.

- Conducting data protection impact assessments (DPIAs) for high-risk processing.

Best Practices for Secure Remote KYC

Build trust from the first click by combining robust remote identity verification, biometric checks, and fraud prevention into your remote KYC process.

Strengthen compliance and customer onboarding with secure digital identity verification, AML screening, and risk-based authentication strategies tailored for remote onboarding KYC.

Use Risk-Based Verification Workflows

A risk-based verification workflow ensures that remote KYC processes adapt to customer risk levels, applying enhanced due diligence (EDD) for higher-risk individuals, jurisdictions, or products while keeping onboarding simple for low-risk users. By using risk scoring, geographic indicators, and regulatory requirements, businesses can improve AML compliance and reduce financial crime exposure without harming the customer experience.

Combine Multiple Verification Signals

Effective remote identity verification combines multiple signals, such as document checks, biometrics, device data, and databases, to build a layered defense against fraud. Using diverse data points improves accuracy and strengthens fraud detection compared to relying on a single signal, especially in remote onboarding KYC environments.

Verify Document Authenticity, Not Just Document Data

While OCR technology enables fast extraction of identity data, it does not confirm whether a document is genuine or tampered with. Robust document verification should include authenticity checks such as template matching, security feature analysis, MRZ validation, and database cross-referencing to detect forged or altered documents and ensure reliable identity proofing in remote KYC processes.

Add Liveness and Injection-Attack Controls

To safeguard biometric identity verification, businesses should use liveness detection and injection-attack prevention to spot spoofing attempts like photos, videos, or deepfakes. Combining passive and active checks with device signals helps confirm the user is present and reduces impersonation risk in remote identity verification workflows.

Provide Manual Review Paths

Even with automation, some cases still need human judgment. Escalating flagged applications to compliance analysts helps ensure accurate decisions and prevents legitimate customers from being wrongly rejected while maintaining KYC compliance in remote onboarding KYC processes.

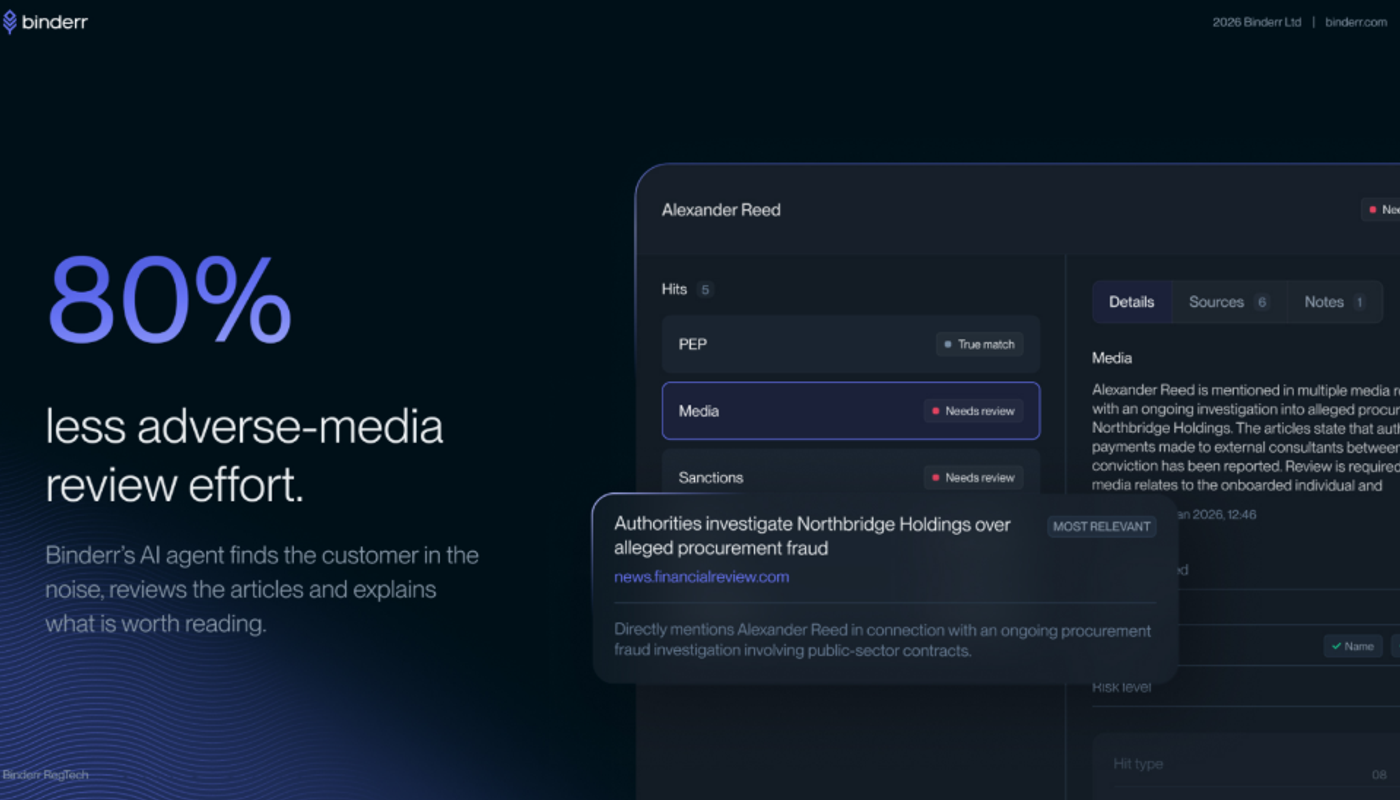

Reduce the Work Behind Adverse Media Reviews

Adverse media searches frequently return large volumes of irrelevant or weakly connected articles. Binderr’s AI-assisted review helps identify whether an article relates to the screened customer, surfaces the most relevant information and explains why the result may require attention. This allows analysts to spend more time making risk decisions and less time reviewing unrelated news results.

(Binderr’s AI-assisted adverse media screening highlights relevant articles and explains why they matter.)

Conduct Vendor Due Diligence

Selecting a remote KYC provider requires vendor due diligence to assess document coverage, biometric accuracy, security, data protection, and regulatory alignment. Businesses should also review performance, reliability, audit trails, and incident response to ensure secure and compliant remote identity verification.

Binderr: Complete Remote KYC and Compliance Solution

Binderr provides an end-to-end compliance platform that goes beyond identity verification:

- KYC and biometric identity verification

- KYB business verification and registry checks

- AML screening across global databases

- Dynamic risk scoring and automated decisions

- UBO identification and ownership mapping

- CDD and EDD workflow automation

Bottom Line

Remote KYC and remote identity verification enable fast, scalable customer onboarding without in-person checks. They improve efficiency and user experience but require strong security, data protection and fraud controls.

An effective remote onboarding KYC approach combines document checks, biometrics, liveness detection, AML screening and risk assessment, supported by ongoing monitoring to maintain compliance and detect emerging risks.

Binderr Compliance helps businesses create secure remote onboarding KYC journeys by bringing KYC, AML screening, risk assessment and ongoing monitoring into one connected platform.