An AML audit is a critical tool for testing whether an organisation’s anti-money laundering programme truly works in practice. It evaluates how well AML controls are designed, implemented, and executed across customer onboarding, risk assessment, and ongoing monitoring. A strong AML audit checklist helps businesses identify gaps early, strengthen compliance frameworks, and reduce exposure to financial crime risks.

Regulators and auditors go beyond reviewing written AML policies. They examine real customer files, KYC records, transaction monitoring alerts, sanctions screening results, and suspicious activity reports to verify that controls operate effectively. According to the United Nations Office on Drugs and Crime, between 2 percent and 5 percent of global GDP is laundered each year, highlighting the importance of robust AML auditing and accurate risk-based controls.

This guide provides a practical AML audit checklist covering governance, AML risk assessment, KYC, CDD, EDD, beneficial ownership verification, sanctions screening, transaction monitoring, suspicious activity reporting, training, record keeping, technology, and remediation.

Try Binderr AML Compliance Software

Binderr Compliance Platform helps businesses streamline AML audits and compliance processes with:

- KYC (Identity Verification) with AI-powered document checks and biometric verification

- KYB (Business Verification) with global registry access and ownership mapping

- AML Screening across sanctions, PEPs, watchlists, and adverse media

- Ongoing AML Monitoring with real-time alerts

- Dynamic Risk Assessment with automated scoring

- UBO Identification and ownership structure visualisation

- Centralised audit trails and compliance reporting

What Is an AML Compliance Audit?

An AML compliance audit is an independent, risk-based review of how well an organisation’s anti-money laundering programme is designed and operating. It goes beyond policies to check whether controls like KYC, CDD, EDD, sanctions screening, and transaction monitoring actually work in practice.

In simple terms, it assesses whether a business meets AML audit requirements and can effectively detect and manage financial crime risks.

A typical AML audit checks:

- Whether relevant laws and regulations are identified and applied

- Whether policies reflect the organisation’s real risk profile

- Whether staff follow procedures consistently

- Whether AML systems are properly configured and effective

- Whether issues and suspicious activity are escalated and resolved

- Whether senior management receives accurate compliance reporting

The FFIEC defines independent testing as a review of compliance relative to risk and an assessment of overall programme effectiveness.

Internal Review vs Independent AML Audit

Internal reviews are ongoing checks by the compliance team, focusing on daily controls like KYC files, alerts, and reporting. They are useful but may lack full objectivity. An independent AML audit provides a more objective assessment of the entire programme, testing both control design and effectiveness as part of structured AML auditing.

Independent testing may be done by:

- Internal audit teams

- External auditors or consultants

- Qualified staff not involved in the controls

- Shared audit resources (where allowed)

Auditor independence is essential. Those reviewing controls should not be responsible for designing or operating them, to avoid conflicts of interest and ensure reliable results.

Why Are AML Audits Important?

Stay ahead of financial crime risks with a proactive AML audit strategy that strengthens compliance and builds trust.

Discover how AML audits, compliance checks, risk assessments, and regulatory readiness work together to protect your business and ensure adherence to AML audit requirements.

Identifying Control Weaknesses: AML audit procedures such as file testing and system validation help uncover gaps in compliance controls, including missing KYC documents, inconsistent customer risk ratings, unresolved transaction monitoring alerts, weak escalation processes, and outdated customer records that may expose the business to financial crime risk.

Preparing for Regulatory Inspections: Maintaining organised AML policies, audit trails, testing records, and documented remediation actions enables businesses to respond efficiently to regulatory inspections and demonstrate a structured, compliant AML auditing framework when regulators request evidence.

Testing Whether Policies Work in Practice: An AML compliance audit ensures that written policies are not just approved but actively followed, highlighting situations where employees may not consistently apply procedures such as customer due diligence, sanctions screening, or suspicious activity reporting.

Improving Risk-Based Decision-Making: Audit findings provide insight into whether AML resources are aligned with the organisation’s highest-risk areas, helping refine the risk-based approach across customer segments, geographic exposure, products, and transaction activity.

Demonstrating Senior Management Oversight: Board minutes, compliance reports, issue logs, budgets, and remediation tracking all serve as evidence of active AML governance, showing that senior management is engaged in overseeing compliance responsibilities in line with regulatory expectations such as those set by the FCA.

Complete AML Audit Checklist

Stay ahead of regulatory scrutiny with a structured AML audit checklist designed to uncover gaps and strengthen compliance controls.

Explore key AML audit requirements, compliance checks, and control testing steps to ensure your anti-money laundering programme is audit-ready and effective.

1. AML Governance and Senior Management Oversight

Strong AML governance forms the foundation of an effective AML compliance audit. Auditors assess whether senior management and the board actively oversee the anti-money laundering programme, ensuring accountability, transparency, and alignment with AML audit requirements. Clear assignment of AML responsibilities, including the appointment of a qualified MLRO, is essential for demonstrating control ownership and regulatory compliance.

From an AML audit checklist perspective, governance reviews focus on whether reporting structures, escalation procedures, and compliance resources are proportionate to the organisation’s risk profile. Effective oversight ensures that AML risks are identified early, escalated appropriately, and addressed through strategic decision-making. Regulators expect senior management to receive regular AML reports and actively participate in compliance oversight.

2. Business-Wide AML Risk Assessment

A business-wide AML risk assessment is a core requirement in any AML compliance checklist, as it determines how effectively an organisation identifies and manages financial crime risks. Auditors evaluate whether the risk assessment captures key risk factors such as customers, jurisdictions, products, services, and delivery channels, while also incorporating emerging threats like terrorist financing and proliferation financing.

An effective AML risk assessment should distinguish between inherent and residual risks and clearly map controls to identified exposures. From an AML audit perspective, the methodology must be consistent, explainable, and regularly updated to reflect changes in business operations or AML audit requirements. Senior management approval is critical to demonstrate ownership and accountability.

Cut compliance time. Screen and detect risk for FREE.

3. AML Policies, Procedures, and Internal Controls

AML policies and procedures translate regulatory requirements into operational controls, making them a critical focus area in any AML audit checklist. Auditors assess whether policies are current, approved, and aligned with applicable AML audit requirements, as well as whether they accurately reflect how controls operate in practice. A disconnect between documented procedures and actual processes is a common AML audit finding.

Effective internal controls ensure consistency in AML compliance activities such as KYC, transaction monitoring, and suspicious activity reporting. Policies should clearly define responsibilities, escalation processes, and customer acceptance criteria, while also addressing prohibited relationships and high-risk scenarios. Regular updates and accessibility for staff are essential for maintaining compliance effectiveness.

4. Customer Identification and KYC Controls

Customer identification and KYC controls are central to any AML compliance audit, as they form the first line of defence against financial crime. Auditors evaluate whether customer identity verification processes are robust, accurate, and completed before onboarding. This includes reviewing document validation, biometric verification, and controls for non-face-to-face onboarding scenarios.

From an AML audit checklist perspective, KYC controls must ensure that customer records are complete, up to date, and supported by verifiable evidence. Auditors also assess how exceptions, failed verifications, and manual overrides are handled, as these areas often present elevated risk. Effective KYC processes help prevent identity fraud, detect synthetic identities, and support ongoing AML monitoring.

5. KYB and Beneficial Ownership Verification

Know Your Business (KYB) and beneficial ownership verification are critical components of any AML audit checklist, ensuring that legal entities are properly identified and their ownership structures are transparent. Auditors should assess whether the organisation verifies company registration details using reliable and independent sources, such as official registries, and whether it accurately identifies ultimate beneficial owners (UBOs) in line with regulatory thresholds. This includes reviewing complex ownership chains, nominee arrangements, and layered corporate structures that may obscure true control.

Effective KYB processes should also include ongoing monitoring of ownership changes and periodic re-verification of entity data. Auditors will expect to see documented ownership charts, UBO declarations, and evidence of verification checks. Weaknesses in KYB and UBO identification can expose businesses to significant financial crime risks, making this a high-priority area in any AML compliance audit.

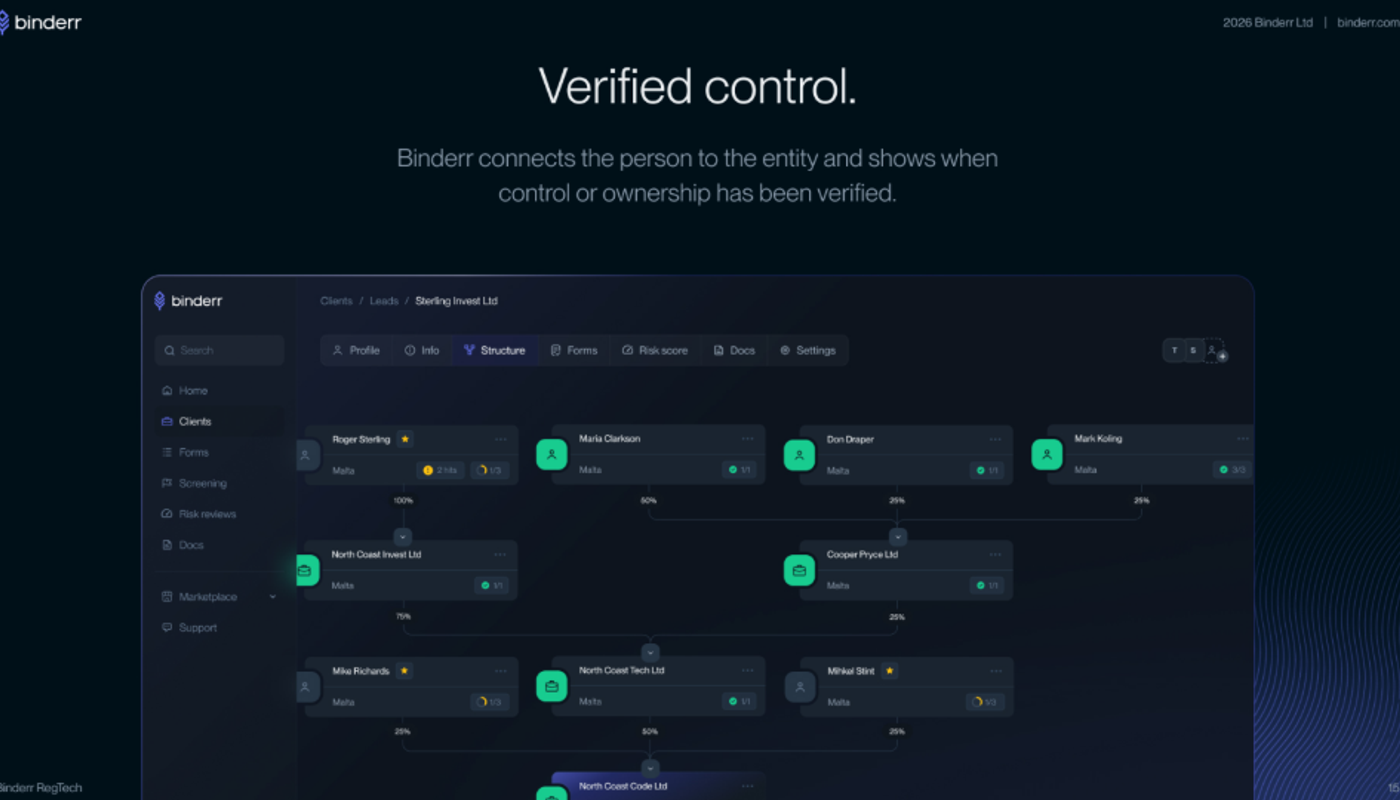

Complex ownership structures can make KYB audits difficult when shareholder, director, and UBO information is stored across separate files. Binderr Compliance maps people and entities within one ownership structure, helping compliance teams verify control, identify missing checks, and produce clearer beneficial ownership evidence during an AML audit.

(Verified ownership and control in Binderr: Connect individuals to legal entities, visualise ownership structures, and see which relationships have been verified.)

Verify UBOs instantly & automate your KYB process.

6. Customer Due Diligence and Risk Rating

Customer Due Diligence (CDD) and risk rating form the foundation of a risk-based AML programme. During an AML audit, reviewers will examine whether each customer has been assigned a documented risk rating based on consistent criteria, including customer type, geographic exposure, products used, and transaction behaviour. The methodology used to calculate risk scores should be transparent, explainable, and aligned with the organisation’s business-wide risk assessment.

Auditors will also assess whether risk ratings are actively used to determine the level of monitoring, frequency of reviews, and escalation requirements. Evidence such as customer risk profiles, approval records, and override logs should demonstrate that risk decisions are justified and consistently applied. Inadequate or unsupported risk ratings are a common AML audit finding and can undermine the effectiveness of the entire compliance framework.

7. Enhanced Due Diligence

Enhanced Due Diligence (EDD) is required for high-risk customers and situations where standard CDD measures are insufficient. An AML audit will evaluate whether clear triggers for EDD are defined, such as politically exposed persons (PEPs), high-risk jurisdictions, complex ownership structures, or unusual transaction patterns. Auditors will also review whether additional checks, including source of funds and source of wealth verification, are conducted thoroughly and documented appropriately.

Strong EDD processes should include senior management approval, enhanced monitoring, and more frequent periodic reviews. Evidence such as EDD reports, adverse media findings, and escalation records should demonstrate that high-risk relationships are subject to increased scrutiny. Failure to apply EDD consistently is a significant compliance gap and may lead to regulatory penalties.

8. Sanctions, PEP, and Adverse Media Screening

Sanctions screening, PEP screening, and adverse media checks are essential controls for identifying high-risk individuals and entities. During an AML compliance audit, auditors will assess whether screening is conducted at onboarding and on an ongoing basis, and whether all relevant parties including beneficial owners, directors, and authorised signatories are included. The effectiveness of screening systems, including fuzzy matching and list updates, is also a key focus area.

Auditors will review how alerts are handled, including the documentation of false positives, escalation procedures, and decision-making processes. Evidence such as screening logs, match disposition records, and system configuration settings should demonstrate that the organisation can detect and respond to potential sanctions breaches or reputational risks. Weak screening controls or inconsistent alert handling can significantly increase exposure to regulatory enforcement and financial crime risk.

Screen users for FREE in seconds with Binderr

9. Transaction Monitoring

Transaction monitoring is a core component of any AML compliance audit, designed to detect unusual or potentially suspicious financial activity in real time or through retrospective analysis. An effective AML transaction monitoring system should align with the organisation’s risk-based approach, taking into account customer profiles, transaction types, geographic exposure, and product risk. Auditors will assess whether monitoring rules, thresholds, and scenarios are appropriately calibrated and supported by documented rationale.

During an AML audit, reviewers typically examine alert generation, investigation workflows, and case management processes. This includes verifying that alerts are reviewed within defined timelines, escalated where necessary, and supported by clear documentation. Data integrity is also critical, so auditors will test whether transaction feeds are complete and accurate, and whether system changes are properly validated. Weaknesses in transaction monitoring can lead to missed suspicious activity, making this a high-risk area in any AML compliance checklist.

10. Suspicious Activity Reporting

Suspicious Activity Reporting (SAR) or Suspicious Transaction Reporting (STR) is a key regulatory obligation that ensures potential financial crime is reported to the relevant authorities. An AML audit will evaluate whether employees can identify suspicious behaviour, escalate concerns internally, and support investigations with sufficient evidence. The audit also checks whether SARs or STRs are filed accurately, completely, and within required timelines.

Auditors will review internal escalation logs, investigation files, and reporting decisions to ensure consistency and compliance with AML audit requirements. They will also assess whether decisions not to file a report are properly documented and justified. Maintaining confidentiality and avoiding tipping-off are essential, and any breaches in these areas can result in serious regulatory consequences. Strong SAR and STR processes demonstrate an organisation’s ability to detect and respond to financial crime risks effectively.

11. Ongoing Monitoring and Periodic Reviews

Ongoing monitoring ensures that customer risk profiles remain accurate over time and that changes in behaviour or circumstances are identified promptly. As part of an AML compliance audit, auditors will assess whether periodic reviews are conducted according to the customer’s risk rating and whether trigger events, such as changes in ownership or unusual transaction patterns, are properly investigated.

An effective ongoing monitoring framework includes regular updates to customer due diligence (CDD) records, rescreening against sanctions and PEP lists, and timely completion of overdue reviews. Auditors will also examine whether high-risk customers are subject to enhanced scrutiny and whether monitoring outcomes are documented clearly. Failure to maintain up-to-date customer information can weaken the overall AML programme and increase exposure to financial crime.

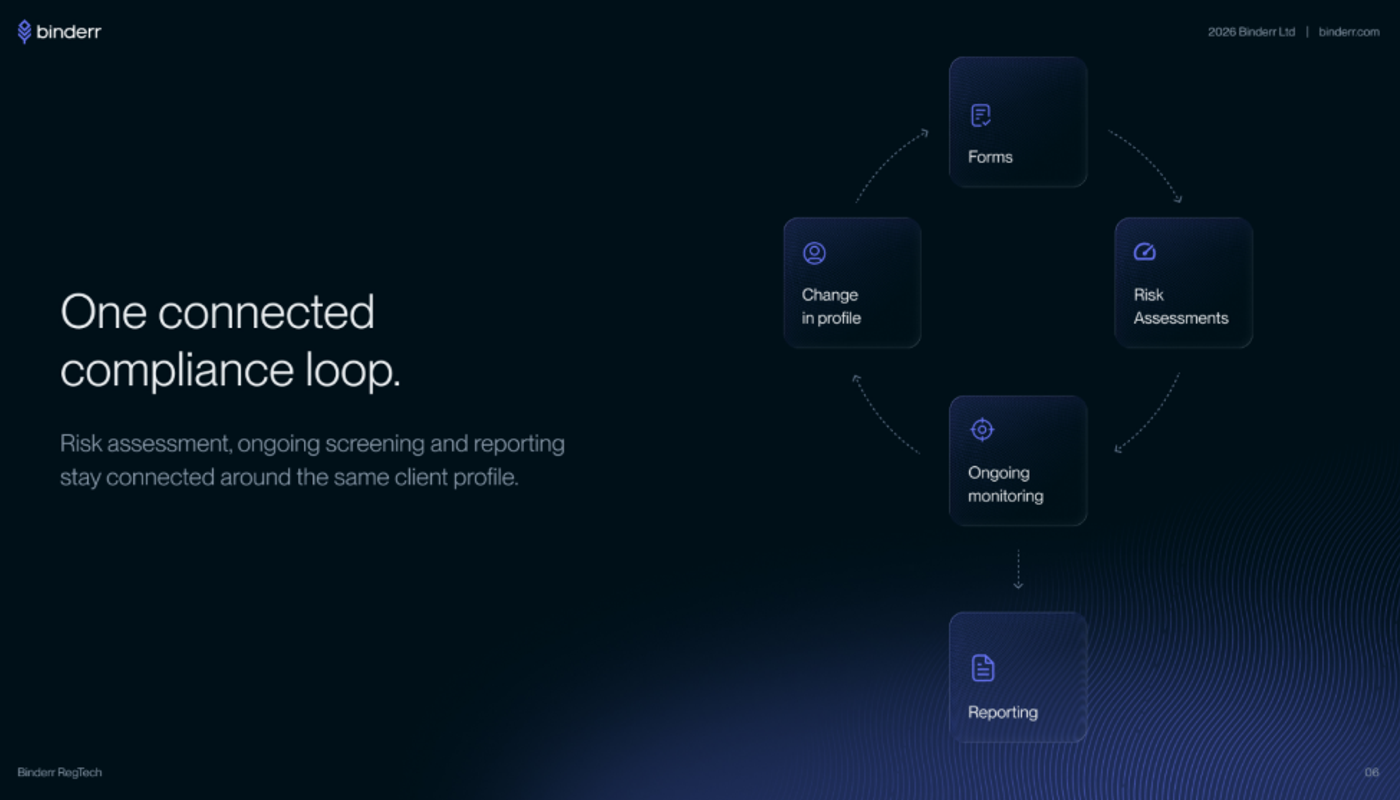

Audit weaknesses frequently arise when onboarding, customer risk assessments, screening alerts, and periodic reviews are managed in separate systems. Binderr creates a connected compliance loop in which new information and customer profile changes can feed into risk assessment, ongoing screening, and reporting without creating disconnected data trails.

(Binderr connects onboarding information, risk assessments, ongoing screening, profile changes, and reporting around the same customer record.)

12. AML Training and Employee Screening

AML training and employee screening are essential for ensuring that staff understand their responsibilities and can effectively implement AML controls. An AML audit will review whether employees receive role-specific training that covers key topics such as KYC, CDD, transaction monitoring, and suspicious activity reporting. Training should be updated regularly to reflect regulatory changes and emerging financial crime risks.

In addition to training, employee screening helps ensure that individuals in sensitive roles meet integrity and suitability standards. Auditors will examine training records, attendance logs, and assessment results to confirm that staff are adequately prepared. They will also review pre-employment and ongoing screening processes where required by regulation. A well-trained workforce is critical to maintaining a strong AML compliance framework and supporting effective AML auditing outcomes.

13. Record Keeping and Audit Trails

Effective record keeping is a core requirement of any AML compliance audit, ensuring that all customer, transaction, and compliance data can be retrieved accurately and promptly. Regulators expect businesses to maintain complete and verifiable records that demonstrate how AML controls were applied, including KYC documentation, transaction histories, and suspicious activity reporting decisions. Strong audit trails allow auditors to trace every action taken, from onboarding to ongoing monitoring, supporting transparency and accountability.

An AML audit checklist should assess whether records are retained for the required regulatory period, protected against unauthorised changes, and easily accessible for review. Businesses should also ensure that audit trails capture key events such as risk rating changes, screening results, and approval decisions. Poor record keeping can lead to compliance gaps, regulatory penalties, and difficulty proving adherence to AML audit requirements during inspections.

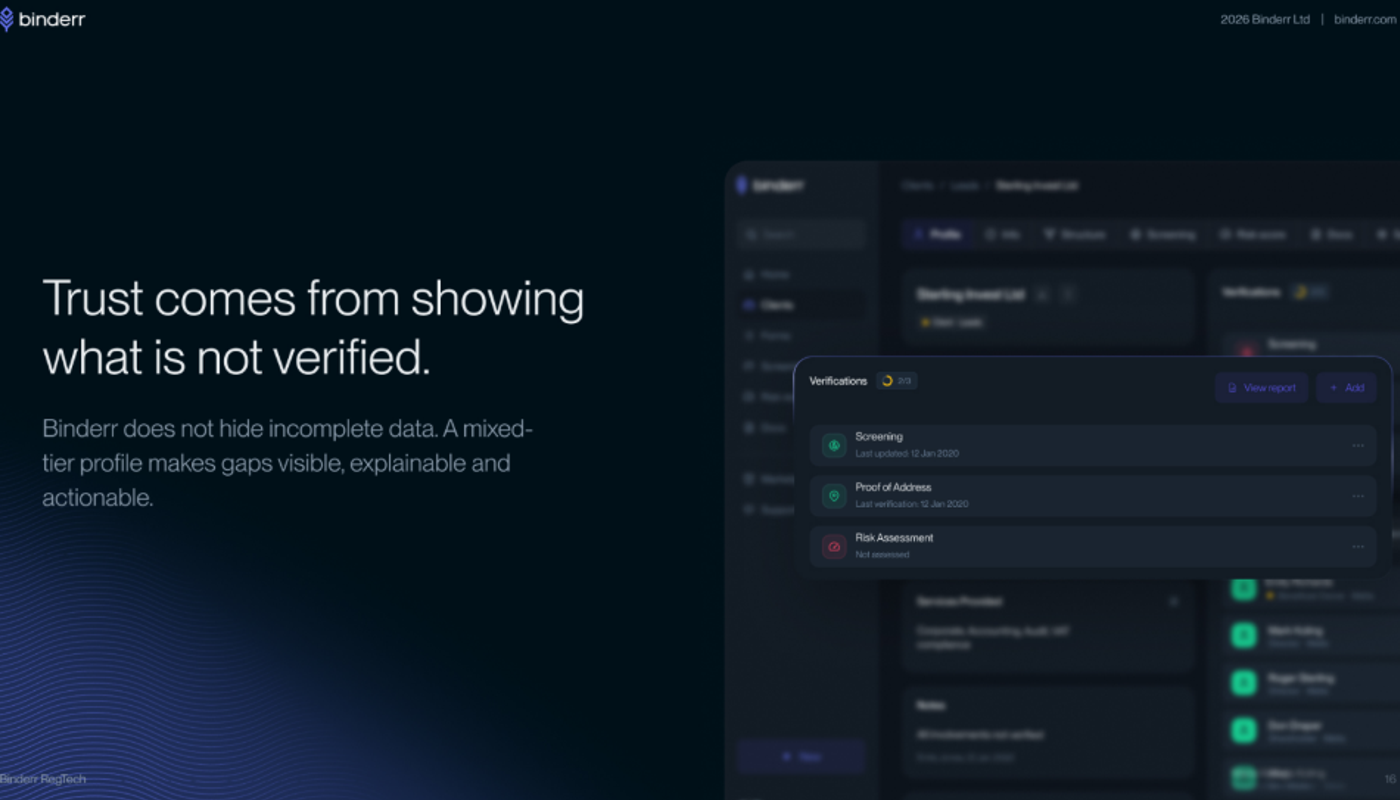

Audit-ready records should show more than completed checks. Auditors may also need to understand which controls were incomplete, when information was last verified, and what action was taken. Binderr makes verification gaps visible and actionable, helping compliance teams identify missing risk assessments, outdated screening results, and incomplete customer evidence before an audit begins.

(Binderr makes completed, outdated, and missing compliance checks visible within the customer profile.)

14. Outsourcing and Third-Party Providers

Outsourcing AML functions to third-party providers can improve efficiency, but it also introduces additional compliance risks that must be carefully managed. During an AML compliance audit, organisations must demonstrate that they have conducted proper due diligence on vendors and that contractual agreements clearly define responsibilities, service levels, and audit rights. Even when outsourcing, the regulated entity remains fully accountable for AML compliance.

An AML audit checklist should include reviewing vendor performance, monitoring service delivery, and ensuring that third-party systems meet AML audit requirements for KYC, sanctions screening, and transaction monitoring. Businesses should also verify that data protection, confidentiality, and business continuity measures are in place. Weak oversight of outsourcing arrangements is a common AML audit finding and can expose organisations to operational and regulatory risks.

15. AML Technology and Data Quality

AML technology plays a critical role in supporting compliance processes, but its effectiveness depends heavily on data quality and system configuration. During an AML audit, auditors assess whether systems used for KYC, transaction monitoring, and sanctions screening are properly configured, regularly tested, and aligned with the organisation’s risk profile. Inaccurate or incomplete data can undermine even the most advanced AML systems, leading to missed suspicious activity or false positives.

An AML audit checklist should evaluate data integrity, system integrations, access controls, and change management processes. Businesses must ensure that data inputs are complete and accurate, system outputs are validated, and any manual overrides are properly documented and monitored. Reliable AML technology, combined with strong data governance, enhances audit readiness and helps organisations maintain effective anti-money laundering controls.

16. Previous Findings and Remediation

Reviewing previous audit findings is essential to determine whether identified AML compliance issues have been effectively addressed. Regulators expect organisations to maintain a structured remediation process, where each finding is assigned an owner, tracked to completion, and supported by evidence. Failure to resolve past issues or repeated findings can indicate weaknesses in governance and control effectiveness.

An AML audit checklist should include verifying that remediation actions are completed within agreed timelines, validated independently, and documented thoroughly. Businesses should also conduct root cause analysis to prevent recurring issues and improve overall AML programme effectiveness. Strong remediation practices demonstrate a proactive approach to compliance and help build confidence with regulators and auditors.

See How Binderr Simplifies AML Audit Processes

Binderr streamlines AML audit preparation and execution by:

- Running KYC, KYB, and AML checks in one platform

- Automatically generating risk scores

- Triggering EDD workflows for high-risk users

- Maintaining complete audit trails

- Centralising compliance data for easy retrieval

This eliminates manual processes and ensures audit readiness at all times.

What Should an AML Audit Report Include?

An AML audit report is a critical document that outlines the findings, risks, and effectiveness of an organisation’s anti-money laundering controls. It provides a structured overview of how well the AML compliance programme aligns with regulatory expectations and highlights areas requiring improvement.

A well-prepared AML audit report should clearly present audit findings, risk ratings, supporting evidence, and actionable recommendations to strengthen AML compliance and ensure regulatory readiness.

Recommend the following structure:

- Executive summary: Provide a concise overview of the AML audit, highlighting key findings, critical risks, and overall effectiveness of the AML compliance programme. This section should give senior management a quick understanding of whether the organisation meets AML regulatory expectations and where immediate attention is required.

- Audit objective: Clearly define the purpose of the AML audit, such as evaluating the effectiveness of anti-money laundering controls or assessing compliance with AML regulations.

- Scope and review period: Outline the areas covered in the AML compliance audit, including business units, systems, and processes reviewed. Specify the time period examined to ensure clarity on the audit coverage.

- Methodology: Explain how the audit was conducted, including document reviews, interviews, walkthroughs, and control testing.

- Overall conclusion: Summarise whether the AML programme is effective, partially effective, or requires significant improvement. Provide a clear statement on the organisation’s compliance posture and risk exposure.

- Detailed findings: Present each identified issue in detail, including control weaknesses in key AML areas. Ensure findings are clearly structured and easy to understand.

- Risk ratings: Assign severity levels such as critical, high, medium, or low to each finding based on regulatory impact and risk exposure.

- Recommended actions: Provide practical remediation steps to address each finding, aligned with AML best practices.

- Action owners: Assign responsibility for each remediation action to specific individuals or departments to ensure accountability.

- Completion deadlines: Set realistic timelines for resolving each issue, prioritising high-risk findings that require urgent attention.

Binderr: A Complete AML Compliance Solution

Binderr provides a full end-to-end compliance solution:

- KYC and identity verification

- KYB and business verification

- AML screening and monitoring

- Risk scoring and assessment

- UBO identification and ownership mapping

- CDD and EDD workflows

- Compliance reporting and audit trails

Bottom Line

Effective AML audit preparation requires more than maintaining policies. Organisations must show that their AML controls work in practice across KYC, due diligence, screening, monitoring, and reporting, supported by strong governance and clear audit trails.

A risk-based AML audit checklist helps identify gaps early, prioritise remediation, and maintain clear evidence for regulators, auditors, and senior management.

Binderr Compliance brings KYC, KYB, AML screening, risk scoring, ongoing monitoring, and audit-ready records into one platform, helping compliance teams maintain clearer and more defensible workflows.