Client onboarding is one of the most critical moments in a regulated firm’s relationship with its customers. It’s where trust begins, but it also where compliance risk is highest. That’s why effective customer screening is essential.

Whether you're onboarding individual users or business clients, a robust customer screening procedure ensures you know exactly who you're dealing with before granting access to your platform, account, or services.

In this guide, we’ll unpack exactly what customer screening is, why it’s so critical during onboarding, who needs it, when it must be applied, and how to build a modern, compliant customer screening checklist.

What is Customer Screening?

Customer screening also known as AML Screening is a core compliance process used by banks and regulated firms to verify who their customers are and assess associated risks.

Customer Screening process involves checking new and existing customers against various databases, such as sanctions lists, watchlists, PEP lists, and media sources, to detect any links to money laundering, fraud or other financial crimes.

In other words, customer screening means thoroughly vetting each customer to ensure they are not “bad actors” in disguise. By systematically comparing customer identities against official watchlists and adverse media, financial firms ensure they comply with regulations and protect the institution from illicit activity.

Customer screening ensures that a bank or firm “knows exactly who they are dealing with” and can spot any signs of money laundering or fraud.

Binderr AML Screening Solution

As an AI-powered AML Screening software, Binderr embeds automated customer screening directly into your customer onboarding workflow.

Binderr instantly verifies identity documents, screens names against over 11,000 global data sources, detects risk indicators in real time, and monitors clint risk continuously in real time.

Importance of Customer Screening in Banking and AML

Customer screening is essential for banking and AML compliance. Regulations worldwide require banks and financial firms to screen customers at onboarding and on an ongoing basis. This is to ensure criminals cannot exploit the financial system. Effective screening protects the institution from legal and reputational risk.

If the customer screening fails to catch a criminal customer, the business faces severe reputational damage and regulatory penalties. Conversely, if screening is slow or inefficient, it hurts customer experience and costs the firm in time and money.

In a competitive market, a smooth yet thorough client screening process keeps good customers happy while still catching high-risk ones.

Client Screening is also the first line of defence against financial crime. It helps prevent money laundering, terrorism financing and fraud by blocking high-risk customers from entry.

For instance, a customer on an international sanctions list will be flagged immediately, avoiding illegal transactions. Screening also safeguards the firm’s reputation: failing to screen properly can damage trust with regulators, investors and the public.

In practice, firms that proactively screening customers can reduce exposure to financial crime and protect their reputation.

Individual User Screening vs Business Customer Screening

Customer screening applies not only to private individuals but also to legal entities such as corporations, partnerships, and trusts. In both cases, the goal remains the same: to detect potential financial crime risks and comply with AML regulations.

However, the customer screening procedure differs depending on whether you're screening an individual or a business customer.

Individual Customer Screening

Individual customer screening focuses on verifying a person’s identity, background, and risk profile. This includes collecting key identifiers such as:

- Full legal name

- Date of birth

- Residential address

- Government-issued identity documents

- Biometric data (such as facial recognition)

Once verified, the individual is screened against sanctions lists, PEP databases, watchlists, and adverse media. This process helps financial institutions assess whether the individual poses a risk of money laundering, fraud, or other financial crimes.

This type of customer screening in AML is common in retail banking, fintech, and investment platforms. For example, a fintech onboarding a new retail client must ensure the user isn’t a sanctioned individual, a politically exposed person, or mentioned in negative news reports.

By integrating automated tools like Binderr, these checks can be carried out in real time—helping firms meet KYC and AML compliance obligations while enhancing onboarding efficiency.

Read More: What is AML Check?

Read More: What is KYC Verification?

Business Customer Screening (Corporate Screening)

Screening business customers requires a more complex and multi-layered AML approach. Often referred to as KYB (Know Your Business), this process involves:

- Verifying the legal entity (company registration, VAT, and tax ID numbers)

- Identifying and verifying UBOs, directors, shareholders

- Conducting sanctions, PEP, and adverse media checks on all associated individuals

- Assessing the nature and legitimacy of the business activity

- Analysing geographic risk (e.g., if the company is based in or operates within high-risk jurisdictions)

This layer of customer screening in banking is crucial, especially given the widespread use of shell companies and complex corporate structures to launder money or conceal ownership. Criminals often attempt to exploit these corporate veils, making it harder for regulators to trace illicit activity.

A robust business customer screening checklist should therefore include both entity-level and individual-level assessments.

Binderr Corporate Screening Solution

KYB Software like Binderr simplify this by aggregating data from global corporate registries, sanctions lists, and PEP databases, allowing compliance teams to automatically screen all beneficial owners and stakeholders linked to a business entity.

Types of Customer Screening

Customer screening encompasses several different checks and categories. Firms typically screen:

Sanctions and Watchlist Screening

This cross-references customers against official sanctions lists (e.g. OFAC, UN, EU) and high-risk watchlists. Any match (direct or by association) raises a red flag.

For example, if a customer’s name appears on a government sanctions list, the firm must often refuse service. Automated like Binderr screening software can check thousands of such lists instantly.

Read More: What is Sanction Screening?Read More: What is Watchlist Screening?

PEP Screening

A PEP (Politically Exposed Person) is someone with a prominent public role, or a close associate of one. PEPs are considered higher risk due to potential bribery or corruption.

Firms must routinely screen all customers to see if they are PEPs. Businesses need to determine if the customer in question is listed as a PEP, noting even relatives of politicians can trigger this check. PEP Screening is often repeated regularly since someone’s status can change over time.

Read More: What is PEP Screening?

Adverse Media Screening

Adverse Media Screening involves checking negative news sources and media reports for any mention of the customer. Even if someone is not on a formal list, a critical news story (e.g. fraud charges, human rights violations) could indicate risk.

Firms routinely screen customers against negative or adverse news stories published worldwide because this can implicate them in criminal activity. Keeping up with global media even in different languages helps firms detect red flags not captured by lists.

Read More: What is Adverse Media Screening?

Other Specialized Lists

In practice, firms may also consult enhanced lists like Special Interest Persons (SIP), anti-corruption watchlists, law enforcement wanted lists, and more.

The goal is comprehensive coverage: from sanctions lists to subpoenas. Technologies often aggregate over 10,000 data sources (as Binderr does) to ensure no list is overlooked. By layering these AML checks, regulated firms achieve a 360° view of customer risk.

Individuals and companies are screened against both static watchlists (sanctions, PEP) and dynamic sources (current events), which is why screening is sometimes also called “enhanced due diligence.”

Customer Screening Procedure and Checklist

A robust customer screening procedure consists of multiple steps. Banks and compliance teams generally follow a checklist that includes:

- Identity Verification (CDD – Customer Due Diligence): Confirm the customer’s identity at onboarding. This means collecting and verifying key details (name, date of birth, address, ID documents) from government IDs or biometric checks. All customers undergo this step to prove they are who they claim to be.

- Enhanced Due Diligence (EDD): If a customer appears higher-risk (e.g. large transactions, obscure background, or name matches alerts), perform deeper checks. This involves researching the customer’s background, business activities, and financial history more thoroughly.

- Sanctions, Watchlist, and PEP Screening: Run the customer’s name and identifiers through global sanctions lists, PEP lists and private watchlists. A match triggers an alert – the compliance team must then determine if a true match exists and whether to proceed (often requiring EDD or rejecting the customer).

- Risk Assessment and Scoring: Based on the above information, assign a risk score or rating to the customer. Factors include the customer’s location, industry, transaction patterns, and known issues. For example, Binderr’s automated tools generate an AI-based risk score for each client, helping compliance teams prioritise reviews.

- Ongoing Monitoring: Customer screening isn’t a one-off. Accounts should be continuously monitored: re-screen customers against updated lists and watch for suspicious transactions. According to Binderr’s process, ongoing monitoring “continuously re-evaluates customer profiles to detect new risks,” including re-screening names and tracking unusual activity.

- Record-Keeping and Reporting: Keep detailed records of each screening check and any decisions or reports filed. If red flags arise, firms file Suspicious Activity Reports (SARs) to regulators. Automated tools also help generate audit-ready compliance reports in one click.

This customer screening checklist ensures that no critical step is missed. Modern AML compliance software often incorporates these steps into an organised workflow or task list.

For instance, Binderr provides a customisable AML checklist feature that allows firms to set up task lists and verification levels, streamlining the compliance process. A thorough checklist also helps satisfy auditors and regulators that the firm has robust screening procedures in place.

Who Needs Customer Screening?

Customer screening is a legal and operational requirement for a wide range of regulated entities, particularly those exposed to financial crime risks.

While it’s most commonly associated with banks, the need for customer screening in AML now extends across many sectors due to tightening global regulations and increasing scrutiny around KYC and AML obligations.

Below is a breakdown of the key sectors and businesses that require customer screening procedures as part of their compliance framework:

Banks and Financial Institutions

Both retail banks and commercial banks are at the forefront of AML enforcement and must conduct robust customer screening in banking. This includes:

- Retail banks

- Investment banks

- Private banks

- Digital challenger banks

- Offshore banks

For these institutions, customer screening AML practices are essential to identify clients who may pose a threat due to links with sanctions, PEPs, or adverse media coverage. Screening helps prevent illicit transactions and ensures compliance with regulations such as the FATF Recommendations, EU AML Directives, and the UK’s Money Laundering Regulations.

Fintechs and EMIs (Electronic Money Institutions)

Digital payment platforms, e-wallet providers, and Electronic Money Institutions (EMIs) are increasingly in scope. Since these services often handle high transaction volumes with minimal human interaction, they are attractive to money launderers.

To mitigate this, EMIs and fintechs must apply a customer screening checklist to every new user—whether an individual or a business. This includes onboarding checks, transaction monitoring, and ongoing risk re-evaluations, all of which are streamlined through platforms like Binderr.

Cryptocurrency Exchanges and Virtual Asset Providers

Under updated FATF guidelines and regional legislation (e.g. EU's MiCA), crypto exchanges, wallet providers, and DeFi platforms are required to implement AML measures, including:

- Sanctions screening

- PEP detection

- KYC and identity verification

- Ongoing monitoring of wallet activity

With the pseudo-anonymous nature of crypto, robust customer screening in AML becomes even more critical. Many crypto platforms now integrate automated screening solutions to flag high-risk users in real time.

Wealth Managers, Asset Managers, and Investment Firms

Firms managing client assets or providing wealth management services must ensure their clients are not involved in criminal activity or sanctioned jurisdictions.

This includes:

- Private equity firms

- Hedge funds

- Family offices

- Pension fund administrators

- Securities dealers

A structured customer screening procedure helps these firms identify politically exposed persons (PEPs), trace fund origins, and remain compliant with AML directives and investor due diligence requirements.

Legal, Accounting, and Corporate Service Providers

Any firm involved in company formation, trust management, or business advisory services must also screen their clients. This is due to the high risk of being used to set up shell entities or move illicit funds.

Such firms include:

- Law firms

- Corporate service providers

- Accountancy and audit firms

- Tax advisors and consultants

These businesses must conduct business customer screening—including the identification and verification of Ultimate Beneficial Owners (UBOs), directors, and shareholders.

Real Estate Agents and Property Platforms

Real estate transactions are a known avenue for laundering illicit funds. As a result, estate agents, property developers, and real estate investment platforms must screen clients especially in high-value transactions.

They must ensure that the source of funds is legitimate and that no parties are linked to criminal networks, sanctioned regimes, or adverse media.

Role of Technology in Automating Client Screening

Technology plays an increasingly vital role in customer screening. Manual checks of AML lists and news sources are too slow and error-prone for today’s volumes. Automation and RegTech platforms speed up screening, reduce human error and ensure consistency.

For example, AI-driven systems can cross-check customer data against thousands of sources in seconds, instead of hours or days. They also reduce false positives; one study found AI-based monitoring can reduce false alerts by up to 40%.

According to industry surveys, adoption of AI and machine learning in AML is booming. PwC reports that 62% of financial institutions use AI/ML for AML today, rising to 90% by 2026.

By 2025 the global RegTech market is projected to be over $22 billion. These systems integrate sanctions feeds, PEP databases, adverse media algorithms and transaction monitoring. They provide real-time alerts so compliance staff can act immediately when a match occurs.

Automation also improves customer experience. Instead of manual lookups, an automated check can instantly clear a legitimate customer or flag a risky one. This reduces onboarding time and friction.

Efficient AML screening software facilitates faster customer onboarding while still protecting the business. In practice, when screening is automated, banks can make decisions in seconds rather than spending days on background research.

In summary, modern screening technology streamlines the entire compliance process: from real-time ID verification and document checks, to instant name-screening against global lists, to continuous monitoring.

Automated AML software ensures regulatory updates (new sanctions, emerging PEPs) are incorporated at once. This allows compliance teams to focus on investigating meaningful alerts rather than compiling data.

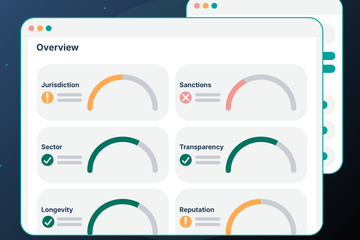

Binderr’s customer onboarding dashboard automatically scores each client’s risk. Colour-coded gauges (green–red) indicate whether a customer is low or high risk, helping compliance officers prioritise reviews.

Bottom Line

Binderr is a modern KYC/KYB/AML platform that illustrates how advanced tools can aid customer screening. Binderr’s AML Screening solution offers end-to-end automation and features tailored to regulated firms.

In essence, Binderr’s solution embeds the entire customer screening procedure in one dashboard. It accelerates each phase – from KYC to sanctions and media checks – through automation and a unified interface.

This means compliance teams can onboard customers faster while still applying full due diligence. Binderr offers real-time AML checks with unmatched speed and accuracy, which helps businesses stay compliant and avert financial crime.

Overall, technology like Binderr offers major benefits: higher accuracy and consistency in screening, faster customer onboarding, and better resource allocation (focusing human review only on genuine risks).