-1400x800.jpg?w=3840&q=75)

As a leading gateway for international finance, Luxembourg supports a vast network of banks, investment funds, fintech companies, insurance providers, and corporate service firms. With billions of euros moving through its financial system every day, AML compliance in Luxembourg plays a vital role in protecting businesses from money laundering, terrorist financing, and other forms of financial crime. Strong anti-money laundering compliance Luxembourg measures help organisations maintain trust, meet regulatory obligations, and operate confidently in global markets.

Built on a combination of national legislation, European Union anti-money laundering directives, and international standards established by the Financial Action Task Force (FATF), Luxembourg’s AML framework is designed to address evolving financial crime risks. According to the Association of the Luxembourg Fund Industry (ALFI), Luxembourg is the largest investment fund centre in Europe and the second largest globally after the United States.

This guide explains the key AML regulations Luxembourg organisations must follow, outlines essential compliance processes, and explores how modern AML compliance solutions can streamline operations while reducing risk.

Binderr AML Compliance Software for Luxembourg Businesses

Managing AML compliance manually can be time-consuming and increase the risk of compliance gaps. Modern compliance platforms help automate customer verification, screening, monitoring, and reporting workflows.

- Global KYC and KYB verification

- Sanctions, PEP, and watchlist screening

- Adverse media monitoring

- Automated CDD and EDD workflows

- Ongoing monitoring and real-time alerts

- Full audit trails and compliance reporting

What Is AML Compliance?

At its core, AML compliance is the framework of policies, procedures, and controls that organisations implement to detect, prevent, and report money laundering, terrorist financing, and other financial crimes. It is a key requirement for businesses operating in regulated sectors such as banking, fintech, insurance, investment management, and payment services. AML regulations require firms to verify customer identities, assess risk, conduct customer due diligence (CDD), monitor transactions, and report suspicious activities.

Beyond regulatory compliance, the primary objective of anti-money laundering programmes is to safeguard the integrity of the financial system while promoting transparency and accountability. Effective AML frameworks combine KYC verification, beneficial ownership checks, sanctions screening, PEP screening, and ongoing monitoring to create a comprehensive defence against financial crime. These measures help organisations reduce risk exposure, meet regulatory obligations, protect their reputation, and strengthen customer confidence.

Access Free Binderr Screening Tool

Why AML Compliance Matters in Luxembourg

Luxembourg’s financial success is built on trust, transparency, and strong financial crime prevention measures.

From AML compliance and customer due diligence to KYC verification, sanctions screening, and ongoing monitoring, businesses must meet evolving regulatory expectations to protect their operations and maintain compliance.

Luxembourg's Position as a Global Financial Centre - Luxembourg is one of the world's leading financial centres, serving international banks, investment funds, insurance companies, fintech firms, and wealth management providers. Its strong global presence attracts cross-border business activity, making AML compliance in Luxembourg essential for maintaining trust, transparency, and financial stability.

Growing Regulatory Expectations - Regulators in Luxembourg continue to strengthen anti-money laundering compliance requirements in line with EU directives and international standards. Businesses are expected to implement robust AML controls, conduct customer due diligence, and maintain effective monitoring processes to identify and mitigate financial crime risks.

Increasing Financial Crime Risks - As financial services become more digital and interconnected, organisations face growing exposure to money laundering, terrorist financing, fraud, and sanctions-related risks. Effective AML compliance programmes help businesses detect suspicious activity early and reduce their vulnerability to evolving threats.

Cross-Border Compliance Challenges - Many Luxembourg-based firms operate across multiple jurisdictions, each with its own regulatory requirements and risk factors. Managing KYC, beneficial ownership verification, sanctions screening, and ongoing monitoring across international customer bases can create significant compliance challenges.

Reputational and Financial Consequences - Failure to comply with Luxembourg AML regulations can result in regulatory penalties, enforcement actions, operational restrictions, and reputational damage. Strong AML compliance practices help organisations protect their reputation, maintain customer confidence, and avoid costly compliance failures.

Run Free AML Checks in Minutes with Binderr

Luxembourg AML Regulatory Framework

Navigating Luxembourg’s AML regulatory framework requires a clear understanding of both local legislation and evolving European standards.

From AML laws and customer due diligence requirements to risk-based compliance obligations, Luxembourg AML regulations establish the foundation for effective anti-money laundering compliance across regulated industries.

AML Law of 12 November 2004

The cornerstone of Luxembourg AML compliance is the Law of 12 November 2004 on the fight against money laundering and terrorist financing, as amended over time to reflect evolving European and international standards. This legislation establishes the primary anti-money laundering obligations for regulated entities operating in Luxembourg, including banks, investment firms, insurance companies, payment institutions, virtual asset service providers (VASPs), accountants, lawyers, and other obliged entities.

Under the law, businesses must implement robust AML controls, conduct customer due diligence (CDD), identify and verify beneficial owners, perform ongoing monitoring, maintain records, and report suspicious transactions. The legislation also promotes a risk-based approach, requiring firms to assess and manage money laundering and terrorist financing risks according to the nature of their customers, products, services, and geographic exposure.

EU Anti-Money Laundering Directives

Luxembourg's AML framework is closely aligned with the European Union's Anti-Money Laundering Directives (AMLDs), which establish harmonised compliance standards across EU member states. Over the years, Luxembourg has incorporated key provisions from the Fourth, Fifth, and Sixth AML Directives into national legislation.

These directives introduced significant requirements, including:

- Enhanced customer due diligence procedures

- Beneficial ownership transparency measures

- Stronger sanctions screening obligations

- Increased scrutiny of politically exposed persons (PEPs)

- Expanded AML requirements for virtual asset businesses

- Improved cooperation between financial intelligence units (FIUs)

- Tougher penalties for AML non-compliance

By implementing EU AML directives, Luxembourg ensures that its financial sector remains aligned with broader European efforts to combat financial crime, money laundering, terrorist financing, corruption, and sanctions evasion.

FATF Recommendations

Luxembourg's AML regulations are also heavily influenced by the Financial Action Task Force (FATF), the global standard-setting body for anti-money laundering and counter-terrorist financing measures. FATF's 40 Recommendations provide a comprehensive framework for identifying, assessing, and mitigating financial crime risks.

Key FATF principles reflected in Luxembourg AML requirements include:

- Risk-based customer due diligence

- Beneficial ownership identification and verification

- Ongoing transaction monitoring

- Suspicious transaction reporting (STR)

- Sanctions compliance

- International information sharing

- Internal AML governance and controls

- Employee training and awareness programmes

As an active participant in the international financial system, Luxembourg continuously updates its AML compliance framework to maintain alignment with FATF expectations and global best practices.

AMLA and Future EU AML Reforms

The European Union is entering a new era of AML supervision with the creation of the Anti-Money Laundering Authority (AMLA). AMLA is designed to strengthen consistency across member states, improve supervisory coordination, and enhance the effectiveness of AML enforcement throughout the EU.

Future reforms are expected to introduce:

- A single EU AML rulebook

- More consistent customer due diligence standards

- Enhanced beneficial ownership verification requirements

- Stronger cross-border supervision

- Increased transparency obligations

- Greater scrutiny of high-risk sectors and transactions

- Expanded use of technology and compliance automation

For Luxembourg businesses, these developments will likely increase regulatory expectations while creating greater consistency across European markets. Firms that invest early in scalable AML compliance programmes and automated compliance solutions will be better positioned to adapt to future regulatory changes.

Risk-Based Compliance Approach

A fundamental principle of Luxembourg AML compliance is the risk-based approach. Rather than applying identical controls to every customer, businesses are expected to assess and manage risks proportionately based on customer profiles, transaction behaviour, geographic exposure, ownership structures, and product risk.

A risk-based AML programme typically includes:

- Customer risk assessments

- KYC and KYB verification procedures

- Sanctions screening and PEP screening

- Adverse media screening

- Enhanced due diligence for high-risk customers

- Ongoing monitoring and transaction monitoring

- Periodic compliance reviews

- Comprehensive audit trails

This approach enables organisations to allocate compliance resources more effectively while strengthening financial crime prevention efforts.

Get Free AML Insights Instantly with Binderr

Which Businesses Must Comply with AML Regulations in Luxembourg?

From global financial institutions to emerging fintech innovators, AML compliance in Luxembourg applies to a wide range of regulated businesses operating within the country's financial ecosystem.

Understanding whether your organisation falls under Luxembourg AML regulations is essential for meeting customer due diligence (CDD), KYC, KYB, transaction monitoring, sanctions screening, and ongoing compliance obligations.

Banks and Credit Institutions - Banks and credit institutions are among the most heavily regulated entities under Luxembourg AML regulations. Because they facilitate deposits, lending, international transfers, wealth management, and investment services, they face significant exposure to money laundering and terrorist financing risks.

Investment Firms and Fund Managers - Luxembourg is one of the world's leading investment fund hubs, making AML compliance particularly important for investment firms, UCITS management companies, AIFMs, and fund managers. These organisations must verify investor identities, identify ultimate beneficial owners (UBOs), and assess customer risk profiles.

Payment Institutions and Electronic Money Institutions - Payment institutions and electronic money institutions (EMIs) play a critical role in facilitating digital payments, remittances, and online financial services. Due to the speed and volume of transactions they process, these businesses face elevated financial crime risks.

Insurance Companies - Insurance providers, particularly those offering life insurance and investment-linked products, are subject to Luxembourg AML compliance obligations. Criminals may attempt to use insurance products to conceal illicit funds or move assets across jurisdictions.

Trust and Company Service Providers - Trust and company service providers (TCSPs) are considered high-risk obliged entities because they assist with company formation, trust administration, nominee services, and corporate structuring. These businesses must conduct thorough KYB verification and identify and verify UBOs.

Accountants and Auditors - Accountants, tax advisers, and auditors often have access to sensitive financial information and may become aware of suspicious transactions during the course of their work. As a result, they are subject to anti-money laundering compliance requirements in Luxembourg.

Law Firms and Notaries - Lawyers and notaries can be exposed to money laundering risks when assisting clients with company formations, mergers and acquisitions, real estate transactions, trust arrangements, or financial transactions. Luxembourg AML laws require legal professionals to perform customer identification checks and verify beneficial ownership.

Real Estate Professionals - Real estate agents, brokers, developers, and other property professionals are increasingly scrutinised due to the potential use of property transactions for money laundering purposes. Luxembourg AML regulations require real estate professionals to verify customer identities and assess transaction risks.

Virtual Asset Service Providers (VASPs) - Virtual Asset Service Providers (VASPs), including cryptocurrency exchanges, digital asset custodians, and crypto wallet providers, are subject to growing AML obligations in Luxembourg. Due to the pseudonymous nature of certain digital assets, regulators require strong compliance controls.

Other Obliged Entities - In addition to the sectors listed above, Luxembourg AML requirements apply to a range of other obliged entities depending on the nature of their activities. These may include dealers in high-value goods, certain financial intermediaries, crowdfunding platforms, gambling operators, and businesses involved in handling significant financial transactions.

Key AML Compliance Requirements in Luxembourg

Navigating Luxembourg AML compliance starts with understanding the core obligations that protect businesses from financial crime and regulatory risk.

From customer due diligence (CDD) and beneficial ownership verification to transaction monitoring, AML screening, and ongoing compliance controls, these requirements form the foundation of an effective anti-money laundering programme in Luxembourg.

Establishing a Risk-Based AML Compliance Framework

A risk-based AML compliance framework is the foundation of an effective anti-money laundering programme in Luxembourg. Businesses should assess their exposure to money laundering and terrorist financing risks by evaluating customer types, products, services, transaction volumes, and geographic locations. This approach allows organisations to allocate compliance resources efficiently and apply appropriate AML controls based on the level of risk identified.

A strong framework should include documented AML policies, risk assessments, compliance monitoring procedures, and clear governance structures. By adopting a risk-based approach, firms can strengthen regulatory compliance, improve financial crime prevention efforts, and demonstrate adherence to Luxembourg AML regulations and international AML standards.

Conducting Customer Due Diligence (CDD)

Customer Due Diligence (CDD) is a core AML requirement that helps businesses verify customer identities and understand the nature of customer relationships. During the onboarding process, organisations must collect and validate key information, including identity documents, business details, and beneficial ownership information where applicable.

Effective CDD procedures reduce the risk of onboarding fraudulent or high-risk customers while supporting compliance with Luxembourg KYC requirements. Ongoing reviews and risk assessments ensure customer information remains accurate and up to date throughout the business relationship.

Applying Enhanced Due Diligence (EDD) for High-Risk Customers

Enhanced Due Diligence (EDD) is required when customers present a higher risk of money laundering or financial crime. This may include politically exposed persons (PEPs), customers from high-risk jurisdictions, complex ownership structures, or unusual transaction patterns that warrant additional scrutiny.

EDD measures often involve obtaining source of funds and source of wealth information, conducting deeper risk assessments, and securing senior management approval before establishing or continuing a business relationship. These enhanced controls help organisations mitigate AML risks and meet regulatory expectations.

Identifying and Verifying Ultimate Beneficial Owners (UBOs)

Identifying Ultimate Beneficial Owners (UBOs) is essential for uncovering the individuals who ultimately own or control a company. Businesses must look beyond legal entities and corporate structures to determine who exercises significant ownership or influence over an organisation.

UBO verification supports transparency and helps prevent criminals from hiding behind complex corporate arrangements. Combining KYB verification, ownership mapping, and beneficial ownership screening enables firms to strengthen AML compliance and reduce exposure to financial crime risks.

Implementing Ongoing Customer Monitoring

AML compliance does not end after onboarding. Ongoing customer monitoring ensures that customer profiles, risk ratings, and business activities remain consistent with the information collected during due diligence procedures.

Regular reviews, automated alerts, and continuous AML screening help identify changes in customer behaviour, ownership structures, or risk levels. This proactive approach enables businesses to respond quickly to emerging threats and maintain compliance with Luxembourg AML requirements.

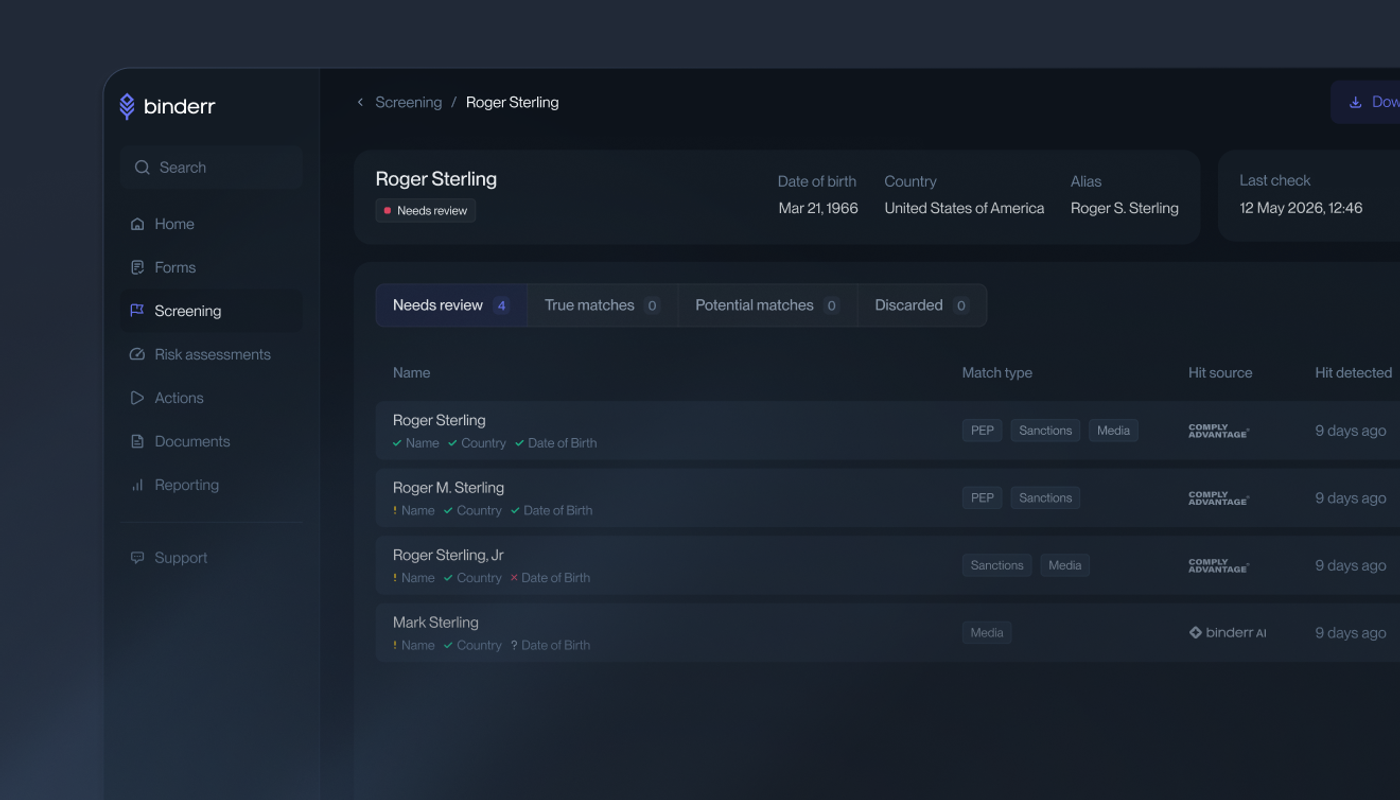

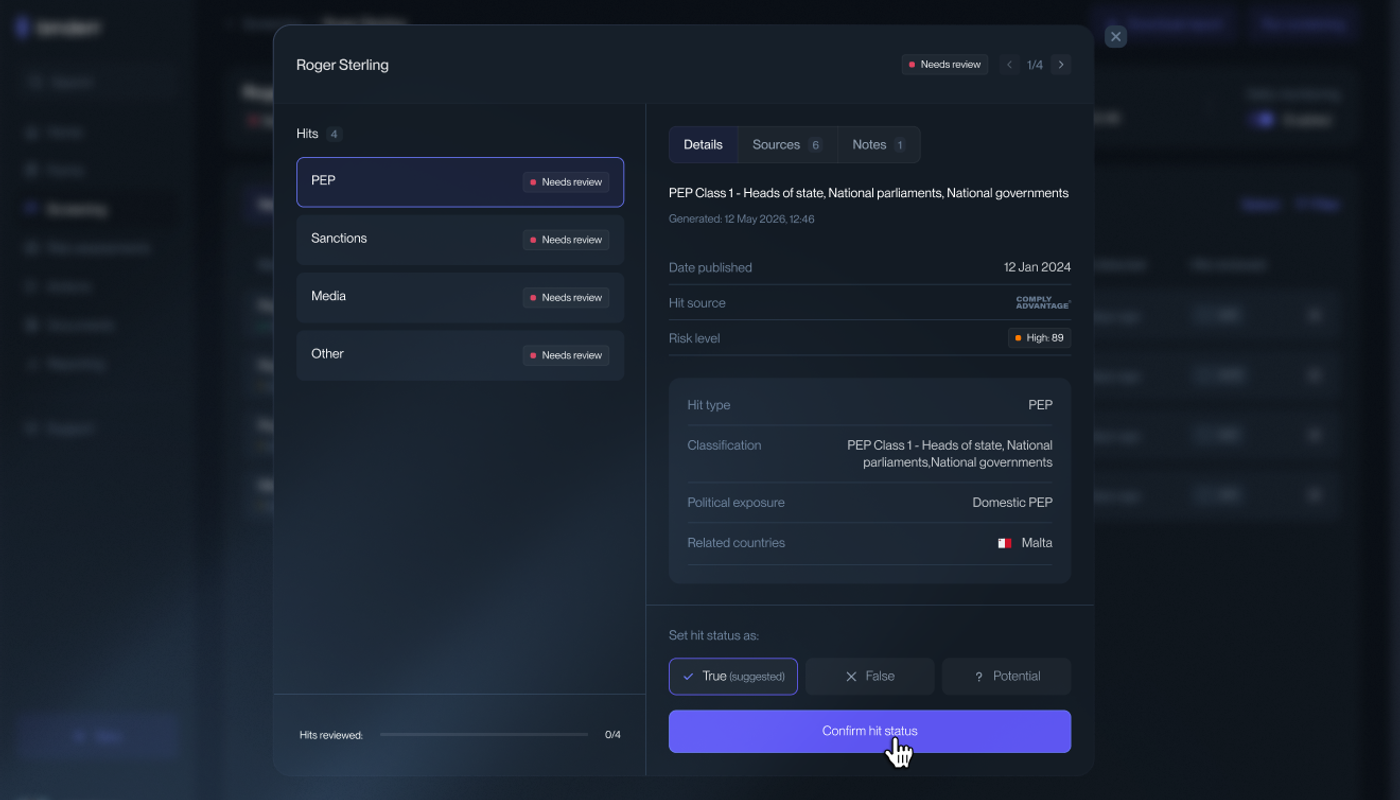

(Binderr allows compliance teams to screen individuals and organisations against global sanctions, PEP databases, watchlists, and adverse media sources from a single workflow. Customer information can be screened during onboarding and throughout the customer lifecycle.)

Monitoring Transactions for Suspicious Activity

Transaction monitoring plays a critical role in detecting unusual or potentially suspicious financial activity. Businesses should implement monitoring systems capable of identifying patterns such as large cash movements, rapid transfers, unusual account activity, or transactions involving sanctioned jurisdictions.

When suspicious activity is detected, compliance teams must investigate alerts, document findings, and determine whether a Suspicious Transaction Report (STR) should be filed. Effective transaction monitoring strengthens AML controls and supports financial crime prevention efforts.

Meeting AML Record-Keeping and Documentation Obligations

Luxembourg AML regulations require businesses to maintain accurate records of customer due diligence, transaction histories, risk assessments, and compliance decisions. Proper documentation creates a clear audit trail and demonstrates compliance during regulatory inspections or audits.

Maintaining organised and accessible records also supports internal investigations and ongoing monitoring activities. Digital compliance platforms can simplify record retention while ensuring documentation remains secure and readily available when needed.

Strengthening Internal Controls and Compliance Governance

Strong internal controls are essential for managing AML risks and ensuring consistent compliance across the organisation. Businesses should establish clear responsibilities, independent oversight functions, escalation procedures, and regular compliance reviews.

Effective governance frameworks help senior management and compliance officers monitor AML performance, address weaknesses, and adapt controls to evolving regulatory requirements. A culture of accountability strengthens overall AML compliance and risk management.

Delivering Effective AML Training and Awareness Programs

AML training ensures employees understand their responsibilities in detecting and preventing money laundering activities. Training programmes should cover customer due diligence, sanctions screening, suspicious activity reporting, transaction monitoring, and emerging financial crime risks.

Regular AML awareness initiatives help staff stay informed about regulatory changes and evolving criminal tactics. Well-trained employees are often the first line of defence against financial crime and play a vital role in maintaining a strong AML compliance programme.

Streamline AML Processes from Onboarding to Monitoring with Binderr

With Binderr Compliance, you can;

- Automate customer onboarding

- Integrate KYC, KYB, and AML screening

- Implement dynamic risk assessment workflows

- Automate enhanced due diligence (EDD) triggers

- Enable continuous monitoring and real-time alerts

- Maintain centralised compliance records for audit readiness

How to Build an AML Compliance Programme in Luxembourg

Build a resilient AML compliance programme that helps your business stay ahead of financial crime risks while meeting Luxembourg AML regulations.

From customer due diligence and KYC verification to ongoing monitoring and AML screening, a structured compliance framework is essential for maintaining regulatory compliance and operational efficiency.

Conduct Risk Assessments

A strong AML compliance programme in Luxembourg begins with a comprehensive risk assessment. Businesses should identify and evaluate money laundering and terrorist financing risks associated with their customers, products, services, delivery channels, and geographic exposure. This risk-based approach helps organisations allocate compliance resources effectively and focus enhanced scrutiny on higher-risk relationships.

Risk assessments should be documented, regularly reviewed, and updated whenever significant business changes occur. By understanding customer risk profiles and emerging financial crime threats, firms can build more effective AML controls, strengthen regulatory compliance, and meet Luxembourg AML requirements with greater confidence.

Implement AML Policies

Clear and well-documented AML policies provide the foundation for a successful compliance framework. These policies should outline procedures for customer due diligence (CDD), enhanced due diligence (EDD), sanctions screening, suspicious transaction reporting, record keeping, and ongoing monitoring.

Effective AML policies ensure consistency across the organisation and help employees understand their compliance responsibilities. Luxembourg businesses should regularly review policies to reflect regulatory updates, evolving risks, and changes in operational processes, ensuring continued alignment with AML regulations.

Deploy Screening Controls

AML screening controls help businesses identify customers and entities that may pose elevated financial crime risks. Screening should include sanctions screening, politically exposed person (PEP) checks, adverse media screening, and watchlist monitoring during onboarding and throughout the customer lifecycle.

Modern AML compliance solutions automate screening processes and reduce the burden of manual reviews. Continuous screening enables organisations to detect risk changes in real time, helping compliance teams respond quickly to new sanctions, negative news, or regulatory developments.

Train Employees

Employee training is a critical component of any AML compliance programme. Staff should understand how money laundering risks arise, how to identify suspicious behaviour, and how to follow internal AML procedures when concerns are detected.

Regular AML training sessions help create a culture of compliance and ensure employees remain informed about changing regulations and emerging threats. Tailored training for different roles can improve awareness and strengthen an organisation's overall financial crime prevention strategy.

Monitor Customer Activity

Ongoing monitoring allows businesses to assess whether customer behaviour remains consistent with their expected risk profile. Transaction monitoring systems can identify unusual patterns, large transfers, rapid movement of funds, or other indicators that may warrant further investigation.

Continuous monitoring is essential for maintaining AML compliance in Luxembourg. By reviewing customer activity on an ongoing basis, organisations can detect suspicious transactions earlier, apply enhanced due diligence when necessary, and fulfil regulatory reporting obligations more effectively.

Maintain Compliance Records

Accurate record keeping is essential for demonstrating compliance with AML regulations. Businesses should retain customer identification documents, risk assessments, screening results, transaction records, and internal investigation files in accordance with applicable retention requirements.

Well-organised compliance records support audits, regulatory inspections, and internal reviews. Maintaining a complete audit trail also helps firms prove that appropriate AML controls were applied throughout the customer relationship and that compliance decisions were properly documented.

Review and Improve Controls

AML compliance is not a one-time exercise. Businesses should regularly evaluate the effectiveness of their AML controls, screening procedures, monitoring systems, and risk management processes to identify weaknesses and opportunities for improvement.

Periodic reviews, internal audits, and compliance testing help organisations adapt to evolving financial crime risks and regulatory expectations. Continuous improvement ensures that AML programmes remain effective, scalable, and capable of protecting the business from compliance failures and reputational damage.

Penalties for AML Non-Compliance in Luxembourg

Failing to meet AML compliance obligations in Luxembourg can lead to severe financial, legal, and reputational consequences for businesses and regulated entities.

Understanding Luxembourg AML regulations, anti-money laundering compliance requirements, regulatory enforcement actions, and risk management expectations is essential for maintaining compliance and avoiding costly penalties.

Financial Penalties - Businesses that fail to meet AML compliance requirements in Luxembourg may face significant financial penalties. Fines can vary depending on the severity of the breach, the level of negligence involved, and whether the organisation failed to implement adequate anti-money laundering controls, customer due diligence procedures, or monitoring systems.

Regulatory Enforcement Actions - Luxembourg regulators can take a range of enforcement actions against non-compliant firms. These measures may include formal warnings, remediation orders, increased supervisory oversight, and public enforcement decisions designed to encourage stronger AML compliance across regulated sectors.

Licence Restrictions - Serious or repeated AML violations can result in restrictions on a firm's ability to operate. Regulators may impose limitations on certain business activities, suspend authorisations, or, in severe cases, revoke licences altogether if an organisation poses an ongoing financial crime risk.

Criminal Liability - AML breaches can lead to criminal liability for both organisations and individuals in certain circumstances. Where money laundering, terrorist financing, or deliberate non-compliance is identified, directors, senior managers, and other responsible parties may face criminal investigations and prosecution.

Reputational Damage - Beyond regulatory penalties, AML failures can cause lasting reputational harm. Negative publicity, loss of customer trust, investor concerns, and damaged business relationships can have a significant impact on a company's long-term growth and market position.

Recent Enforcement Trends - Recent enforcement trends across Luxembourg and the wider European Union show increased scrutiny of AML programmes, beneficial ownership verification, sanctions screening, and ongoing monitoring controls. Regulators are placing greater emphasis on risk-based compliance frameworks and the use of technology to strengthen financial crime prevention efforts.

Try this Free Screening & Verification Tool by Binderr

Common AML Compliance Challenges

Navigating AML compliance in Luxembourg can feel like aiming at a moving target, where regulations, risks, and customer expectations constantly evolve.

From customer due diligence and sanctions screening to beneficial ownership verification and ongoing monitoring, businesses face a range of AML compliance challenges that require robust controls, efficient processes, and scalable technology solutions.

Manual Compliance Processes - Many organisations still rely on spreadsheets, emails, and disconnected systems to manage AML compliance. Manual processes can slow customer onboarding, increase the risk of human error, and make it difficult to maintain consistent compliance records and audit trails.

False Positives - AML screening tools often generate large numbers of alerts that require review. High volumes of false positives can overwhelm compliance teams, delay onboarding decisions, and divert resources away from investigating genuine financial crime risks.

(Binderr provides detailed source information, risk indicators, match classifications, and investigation workflows that help compliance teams quickly determine whether a screening alert is a true match, false positive, or potential match.)

Complex Ownership Structures - Identifying ultimate beneficial owners (UBOs) can be challenging when businesses operate through multiple entities, trusts, or international holding companies. Complex ownership structures often require additional due diligence and verification to meet Luxembourg AML requirements.

Cross-Border Customers - Luxembourg businesses frequently serve customers across multiple jurisdictions, each with different risk profiles and regulatory considerations. Managing KYC, sanctions screening, and enhanced due diligence for international clients can significantly increase compliance complexity.

Resource Constraints - Smaller compliance teams may struggle to keep up with growing regulatory obligations, customer reviews, and ongoing monitoring requirements. Limited resources can make it difficult to scale AML compliance programmes while maintaining regulatory standards.

Regulatory Change Management - AML regulations continue to evolve at both the Luxembourg and EU levels. Businesses must regularly update policies, procedures, and controls to remain compliant with new requirements, guidance, and enforcement expectations.

Binderr End-to-End AML Compliance Platform

AML compliance requires more than customer verification. Businesses need a complete framework for onboarding, screening, risk assessment, monitoring, and reporting.

- KYC and KYB verification

- AML screening and ongoing monitoring

- UBO discovery and verification

- Dynamic risk scoring and risk assessment

- Automated CDD and EDD workflows

- Compliance reporting with audit-ready records

Bottom Line

AML compliance in Luxembourg helps businesses prevent financial crime and meet regulatory requirements. Organisations must implement measures such as customer due diligence (CDD), KYC and KYB verification, sanctions screening, transaction monitoring, and ongoing risk assessments.

A strong AML programme should follow a risk-based approach to identify and manage money laundering risks. Automated compliance tools can simplify verification, screening, monitoring, and reporting while improving efficiency and accuracy.

By investing in effective AML controls, businesses can reduce risk, maintain compliance, and build trust with regulators and customers. For organisations looking to simplify AML compliance in Luxembourg, Binderr Compliance provides an efficient all-in-one platform for KYC, KYB, AML screening, risk assessment, and ongoing monitoring.