Across the UK economy, organisations are facing growing expectations to combat financial crime and protect the integrity of the financial system. Money laundering remains one of the biggest financial crime threats facing the UK, placing businesses across regulated sectors under increasing pressure to strengthen AML compliance, identify suspicious activity, and prevent criminals from exploiting legitimate services. According to the UK Government, hundreds of billions of pounds are estimated to be laundered through or within the UK each year.

AML compliance in the UK extends far beyond the financial sector. Estate agents, cryptoasset businesses, trust and company service providers, auditors, tax advisers, and many other regulated firms must implement robust controls to detect and prevent financial crime. As criminal methods become more sophisticated, businesses need stronger processes and smarter technology to manage risk effectively.

This guide explains everything you need to know about AML Compliance UK, including the legal framework, customer due diligence requirements, enhanced due diligence, KYC and KYB checks, AML screening, suspicious activity reporting, and best practices for building a modern AML compliance programme.

Binderr AML Compliance Software UK

- KYC identity verification with AI-powered document checks, biometric face matching, and liveness detection

- KYB business verification with access to global company registries and corporate records

- AML screening across sanctions lists, watchlists, PEP databases, and adverse media sources

- Ongoing AML monitoring with real-time alerts for risk changes

- Dynamic risk assessment and automated customer risk scoring

- UBO identification and ownership structure mapping

- Automated CDD and EDD workflows

What Is AML Compliance?

Anti-money laundering (AML) compliance refers to the policies, procedures, controls, and technologies that organisations use to prevent, detect, and report money laundering, terrorist financing, sanctions evasion, and other forms of financial crime. In the UK, AML compliance is a legal requirement for regulated businesses and forms a critical part of a broader financial crime prevention framework.

Money laundering is the process of disguising the origins of illegally obtained funds so they appear to come from legitimate sources. Criminals use money laundering techniques to conceal proceeds generated from activities such as fraud, corruption, drug trafficking, cybercrime, tax evasion, and organised crime.

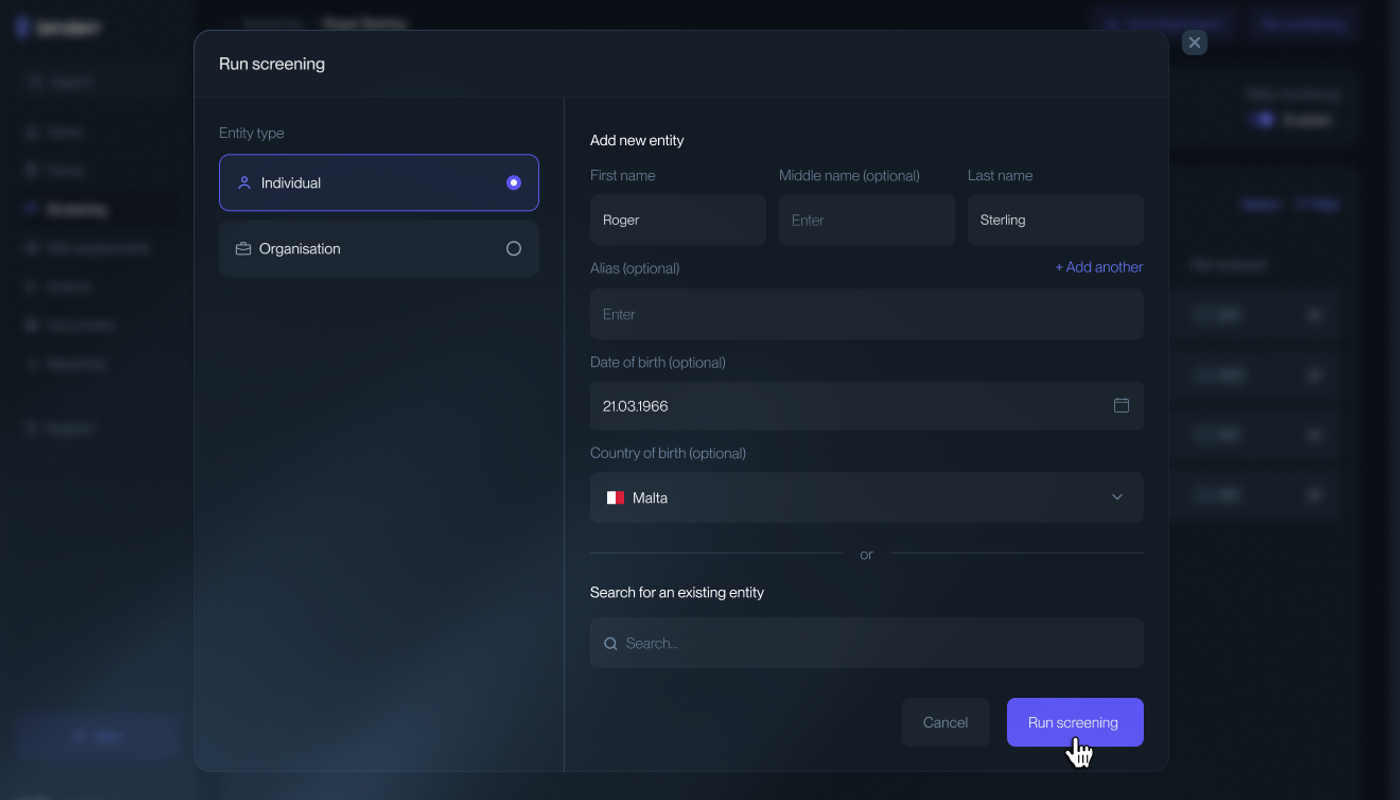

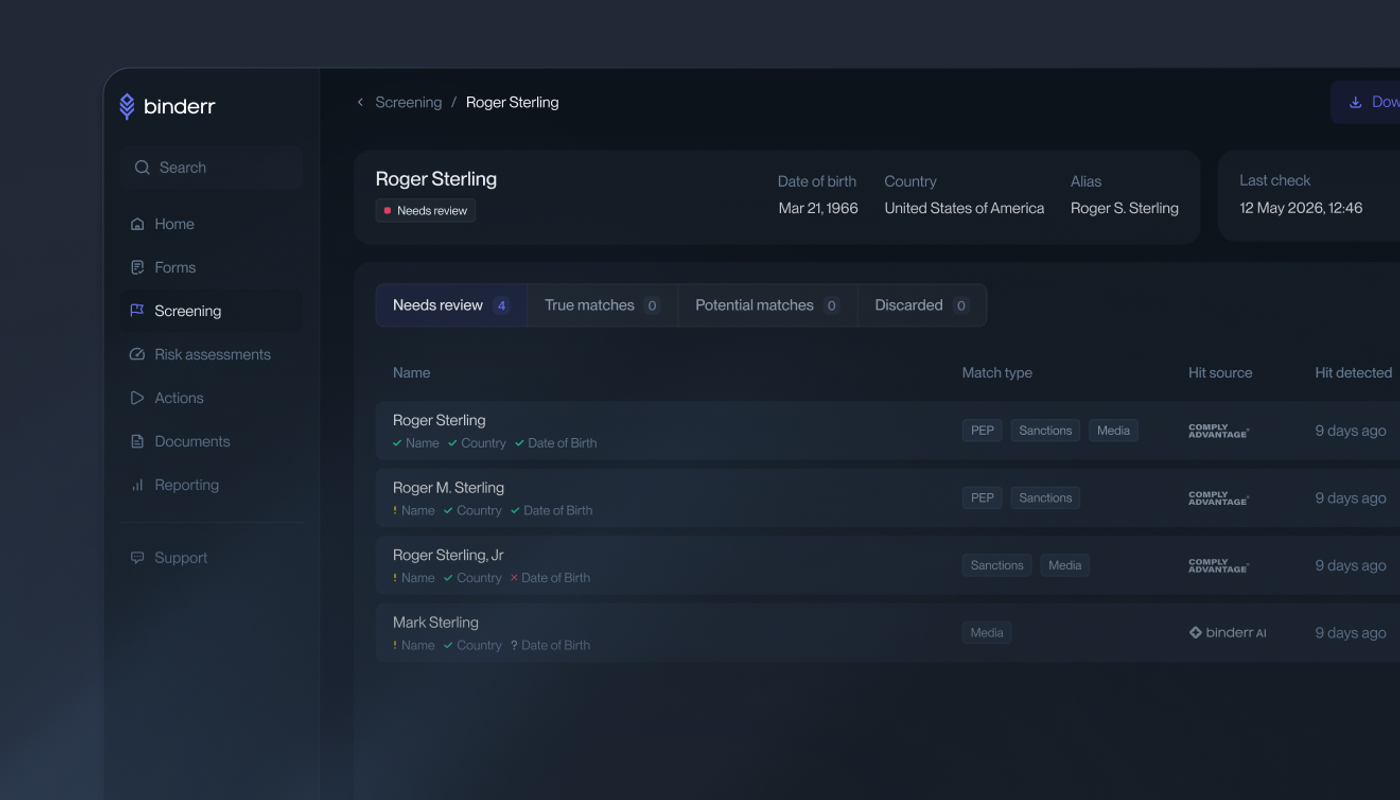

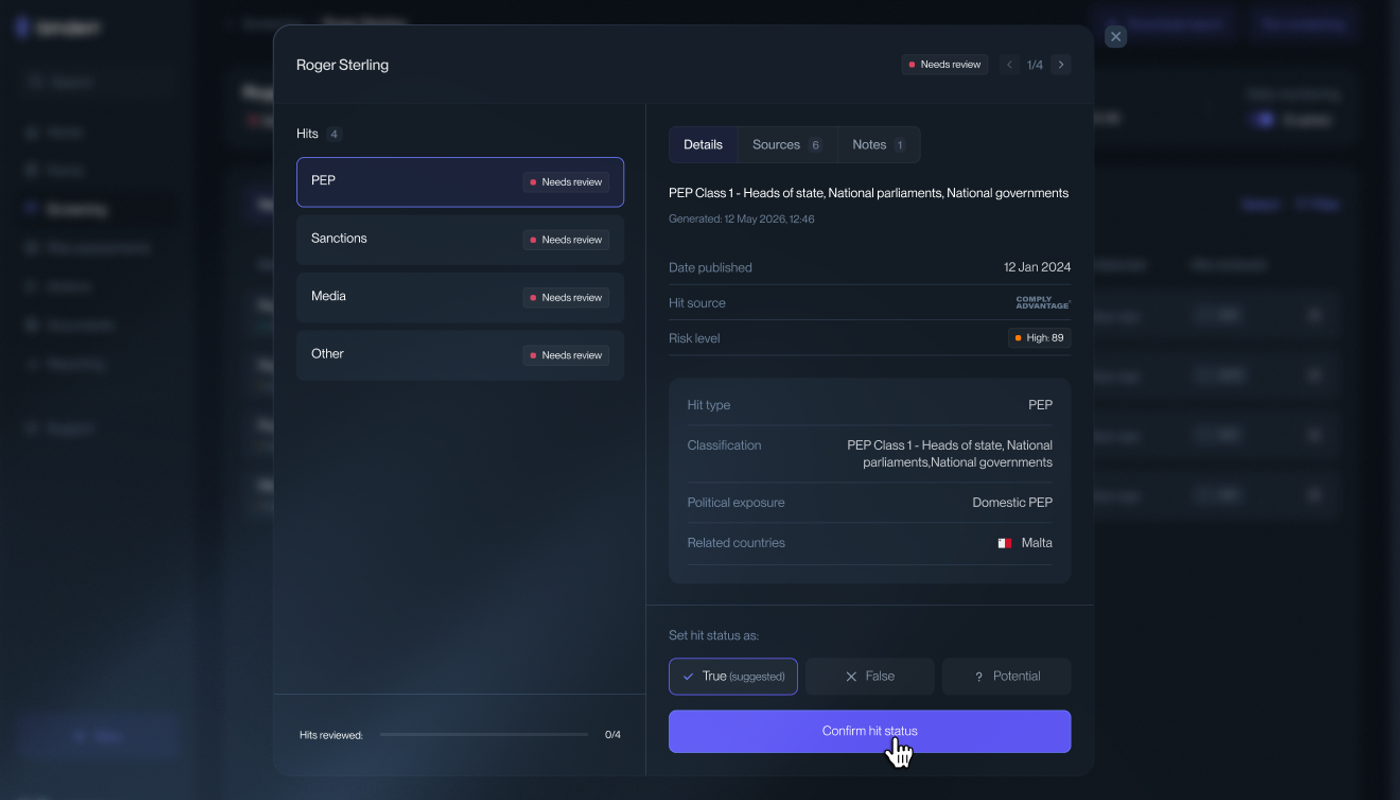

Before businesses can perform sanctions screening, PEP checks, or adverse media monitoring, they must first collect and verify key customer information. Modern AML screening platforms automate this process by allowing compliance teams to screen individuals and organisations against multiple global risk databases in real time.

(Binderr allows compliance teams to screen individuals and organisations against sanctions lists, PEP databases, watchlists, and adverse media sources from a single interface.)

Simplify AML Compliance with Binderr

Binderr helps businesses automate customer onboarding, AML screening, sanctions checks, adverse media monitoring, risk assessments, and ongoing compliance monitoring through a single platform.

With Binderr Compliance, you can;

- Global AML screening coverage

- Sanctions, PEP, and watchlist screening

- Adverse media monitoring

- Automated risk scoring

- Ongoing monitoring and alerts

- Complete audit trails

Understanding the UK AML Regulatory Framework

The UK AML regulatory framework establishes the legal and compliance requirements that regulated businesses must follow to prevent money laundering, terrorist financing, and other forms of financial crime. It combines legislation, regulatory guidance, and supervisory oversight to help organisations identify, assess, and mitigate AML risks.

Understanding UK AML regulations, including the Money Laundering Regulations, Proceeds of Crime Act (POCA), sanctions requirements, and FCA AML expectations, is essential for maintaining effective AML compliance and avoiding regulatory penalties.

Proceeds of Crime Act (POCA)

The Proceeds of Crime Act (POCA) is a key piece of UK AML legislation that helps combat money laundering, terrorist financing, and other financial crimes. Its purpose is to prevent criminals from benefiting from illegal activities by allowing authorities to investigate, seize, and recover criminal assets. Under POCA, regulated businesses must identify and report suspicious activity by submitting Suspicious Activity Reports (SARs) to the National Crime Agency (NCA). In some cases, failing to report suspicious activity can be a criminal offence.

POCA also creates several money laundering offences, including concealing, transferring, acquiring, using, or possessing criminal property. It prohibits tipping off individuals about investigations and actions that could prejudice an investigation after a SAR has been filed. To comply with POCA, businesses should maintain effective customer due diligence (CDD), AML screening, transaction monitoring, and internal reporting procedures. These controls help detect suspicious behaviour, reduce compliance risks, and support adherence to UK AML regulations.

Money Laundering Regulations (MLRs)

The Money Laundering, Terrorist Financing and Transfer of Funds (Information on the Payer) Regulations 2017, commonly known as the Money Laundering Regulations (MLRs), form the core framework for AML compliance in the UK. They require regulated businesses to take a risk-based approach by assessing customer, geographic, product, and delivery channel risks. Key obligations include customer due diligence (CDD), enhanced due diligence (EDD) for higher-risk relationships, beneficial ownership verification, sanctions screening, and ongoing monitoring.

The MLRs also require businesses to maintain effective AML policies, procedures, and controls. Organisations must keep records of customer identification, risk assessments, screening results, and monitoring activities, while providing staff training and conducting regular reviews of AML controls. Following the MLRs helps businesses reduce financial crime risks and meet regulatory expectations from authorities such as the FCA and HMRC.

Terrorism Act

The Terrorism Act complements UK AML regulations by targeting terrorist financing and requiring businesses to identify and prevent transactions that may support terrorist activities. While AML controls focus on money laundering, the Act extends compliance obligations to include detecting suspicious financial behaviour linked to terrorist organisations, individuals, or networks. As a result, customer due diligence, sanctions screening, and transaction monitoring are essential AML controls.

Businesses should ensure their AML programmes can identify unusual payment patterns, high-risk jurisdictions, and individuals on sanctions or terrorism-related watchlists. Suspected terrorist financing must be escalated and reported through the appropriate channels, often via a SAR. Integrating these controls into broader AML monitoring helps organisations meet regulatory requirements and protect the financial system.

Sanctions and Anti-Money Laundering Act (SAMLA)

The Sanctions and Anti-Money Laundering Act (SAMLA) provides the legal basis for the UK's independent sanctions regime after Brexit. It allows the UK government to impose sanctions on individuals, organisations, and countries linked to terrorism, corruption, human rights abuses, and threats to national security. For regulated businesses, SAMLA creates important compliance obligations beyond standard AML requirements.

To comply with SAMLA, organisations must carry out sanctions screening during onboarding and throughout the customer relationship. This includes screening customers, beneficial owners, directors, and counterparties against UK sanctions lists and relevant watchlists. Ongoing monitoring is essential because sanctions can change quickly. Automated screening tools help businesses identify matches faster, reduce compliance risks, and avoid penalties for sanctions breaches.

(Binderr helps compliance teams screen individuals and businesses against global sanctions lists, politically exposed persons (PEPs), watchlists, and adverse media sources. Results are consolidated into a single review workflow, making investigations faster and more accurate.)

FCA AML Guidance

The Financial Conduct Authority (FCA) plays a key role in supervising regulated firms and ensuring effective AML compliance. FCA guidance sets expectations around governance, risk management, customer due diligence, enhanced due diligence, transaction monitoring, and suspicious activity reporting. Firms are expected to take a proportionate, risk-based approach that reflects the nature and complexity of their business.

The FCA also expects firms to maintain audit trails, conduct regular risk assessments, provide staff training, and monitor compliance effectively. Increasingly, the focus is on how well AML controls work in practice rather than whether policies simply exist. Automated screening, ongoing monitoring, and strong risk management frameworks can help businesses demonstrate compliance and respond to regulatory scrutiny.

Get Free AML Insights Instantly with Binderr

Which Businesses Must Comply With UK AML Regulations?

Many organizations operating in regulated sectors must comply with UK AML regulations to prevent money laundering, terrorist financing, and other financial crimes.

Understanding whether your business falls within the scope of anti-money laundering compliance UK requirements is essential for meeting customer due diligence, AML screening, record-keeping, and reporting obligations.

Financial Institutions

Financial institutions are among the most heavily regulated entities under UK AML compliance rules. Banks, Electronic Money Institutions (EMIs), payment institutions, wealth managers, and investment firms must implement robust anti-money laundering controls to detect and prevent financial crime. These organizations are expected to conduct customer due diligence (CDD), perform AML screening, monitor transactions, and report suspicious activity where necessary. Given their exposure to high transaction volumes and cross-border payments, regulators place significant emphasis on effective AML monitoring and risk management.

- Banks

- EMIs

- Payment institutions

- Wealth managers

- Investment firms

Cryptoasset Businesses

Cryptoasset businesses have become a major focus of UK AML regulations due to the potential misuse of digital assets for money laundering and sanctions evasion. Crypto exchanges, custodial wallet providers, and virtual asset service providers (VASPs) must comply with AML requirements, including KYC verification, sanctions screening, transaction monitoring, and ongoing customer risk assessments. As the crypto sector evolves, regulatory expectations continue to increase.

- Exchanges

- Custodians

- Virtual asset providers

Professional Services

Many professional service firms play a critical role in financial transactions and corporate structures, making them subject to AML obligations. Accountants, auditors, tax advisers, and law firms must identify clients, verify beneficial ownership, assess risk levels, and maintain detailed records. These businesses are often involved in company formation, property transactions, and financial planning, which can present elevated money laundering risks if not properly monitored.

- Accountants

- Auditors

- Tax advisers

- Law firms

Trust and Company Service Providers

Trust and Company Service Providers (TCSPs) are required to comply with UK AML requirements because they frequently assist with company formation, nominee services, registered office facilities, and trust administration. These services can be attractive to criminals seeking to conceal beneficial ownership, making KYB checks, UBO verification, and enhanced due diligence essential components of compliance.

Estate Agents and Property Businesses

Estate agents and property-related businesses are subject to AML regulations because real estate transactions can be used to launder large sums of money. Firms operating in this sector must conduct customer due diligence, verify the source of funds where appropriate, and identify suspicious activity. Effective AML checks help reduce the risk of illicit funds entering the UK property market.

Other Regulated Sectors

Several other industries also fall within the scope of UK anti-money laundering regulations. These may include high-value dealers, art market participants, gambling operators, and certain lending or financial service providers. Regardless of sector, businesses must adopt a risk-based approach, implement AML controls, conduct sanctions and PEP screening, and maintain ongoing compliance with evolving regulatory requirements.

The Core Components of an AML Compliance Program

An effective AML compliance programme is built on a risk-based framework that helps businesses identify, assess, and mitigate money laundering and financial crime risks. UK AML compliance requirements expect regulated firms to implement robust controls, customer due diligence procedures, ongoing monitoring, and governance measures that align with their risk exposure.

The following core components form the foundation of a strong anti-money laundering compliance programme and support compliance with UK AML regulations, customer due diligence (CDD), enhanced due diligence (EDD), AML screening, and ongoing monitoring obligations.

Conducting an Effective AML Risk Assessment

An effective AML risk assessment is the foundation of any AML compliance programme. UK businesses should adopt a risk-based approach by conducting an enterprise-wide assessment of exposure to money laundering, terrorist financing, sanctions breaches, and other financial crime risks. This should evaluate customer risk factors such as customer type, ownership structure, transaction behaviour, and geographic exposure to high-risk jurisdictions or sanctioned countries.

Businesses should also assess product and delivery channel risks to identify vulnerabilities in their services and onboarding processes. For example, products that enable rapid fund movement or cross-border transactions may present higher risks, while non-face-to-face onboarding may require enhanced verification. Regular monitoring, documented assessments, and periodic reviews help organisations respond to evolving threats and maintain compliance with UK AML regulations.

Developing Robust AML Policies and Procedures

Clear AML policies and procedures provide employees with a structured framework for meeting regulatory obligations and maintaining consistent anti-money laundering compliance across the organisation. These documents should clearly outline customer due diligence (CDD), enhanced due diligence (EDD), sanctions screening, politically exposed person (PEP) checks, suspicious activity reporting (SARs), record-keeping requirements, and escalation processes for higher-risk cases.

Well-designed AML procedures ensure consistency across departments, reduce compliance gaps, and support a risk-based approach to financial crime prevention. They also demonstrate to regulators such as the FCA and HMRC that appropriate AML controls, governance measures, and compliance frameworks are in place to identify, assess, and manage money laundering and terrorist financing risks effectively.

Implementing Strong Internal Controls

Strong internal controls help businesses detect, prevent, and respond to money laundering risks throughout the customer lifecycle. These controls may include segregation of duties, approval workflows, transaction monitoring systems, customer risk assessments, ongoing monitoring processes, and automated AML screening tools that identify sanctions, PEPs, and adverse media risks.

By implementing effective controls, organisations can strengthen compliance oversight, improve risk management, and create a defensible audit trail that supports regulatory examinations, internal reviews, and independent compliance assessments. Robust internal controls also help reduce operational risk and ensure AML obligations are applied consistently across all business activities.

Delivering Ongoing AML Staff Training

AML compliance is only effective when employees understand their responsibilities and can apply AML procedures correctly in day-to-day operations. Regular AML training helps staff recognise suspicious activity, identify financial crime red flags, understand customer due diligence requirements, and follow internal reporting procedures accurately.

Training programmes should be tailored to specific roles and updated frequently to reflect regulatory changes, emerging threats, sanctions developments, and evolving AML requirements across the UK compliance landscape. Ongoing education helps build a strong compliance culture and ensures employees remain vigilant against money laundering, fraud, and terrorist financing risks.

Independent AML Audits and Compliance Testing

Independent AML audits provide an objective assessment of whether compliance controls, policies, and procedures are operating effectively and in line with UK AML regulations. Regular testing helps identify weaknesses in customer due diligence processes, monitoring systems, sanctions screening programmes, reporting procedures, and overall risk management frameworks.

These reviews support continuous improvement, strengthen governance, and help businesses demonstrate compliance with FCA, HMRC, and other supervisory expectations. Independent audits also provide valuable insights into emerging compliance risks and help organisations address deficiencies before they result in regulatory enforcement actions or financial penalties.

Maintaining Accurate AML Records and Documentation

Accurate record keeping is a core requirement under UK AML regulations and forms a critical part of any AML compliance programme. Businesses must maintain records of customer due diligence checks, beneficial ownership verification, risk assessments, AML screening results, transaction monitoring activities, ongoing monitoring reviews, and suspicious activity reports.

Comprehensive AML documentation supports regulatory inspections, facilitates investigations, and provides evidence that appropriate compliance measures have been applied throughout the customer lifecycle. Maintaining detailed and accessible records also helps organisations demonstrate compliance with the Money Laundering Regulations, respond efficiently to regulator requests, and support effective financial crime risk management.

Streamline AML Processes with Binderr

Building and maintaining an AML compliance programme often requires multiple systems for onboarding, verification, screening, monitoring, and reporting. Binderr simplifies the entire process through a unified compliance platform.

- Run KYC, KYB, and AML checks from one platform

- Automatically calculate customer risk scores

- Trigger CDD and EDD workflows based on risk

- Verify businesses, directors, shareholders, and UBOs

- Screen individuals and entities against sanctions, PEPs, watchlists, and adverse media

- Maintain complete audit trails and compliance records

- Monitor customers continuously for risk changes

Building an Effective AML Risk Assessment Framework

A robust AML risk assessment framework helps businesses identify, evaluate, and mitigate money laundering and financial crime risks across their operations.

By adopting a risk-based approach, organisations can strengthen AML compliance, improve customer due diligence, support ongoing monitoring, and meet UK AML regulatory requirements more effectively.

Assessing Customer Risk Factors

A robust AML risk assessment begins with understanding who your customers are and how their profile may influence money laundering risk. Businesses should evaluate factors such as customer type, occupation, ownership structure, expected account activity, and whether the individual or organisation is a politically exposed person (PEP). High-risk customers may include those with complex corporate structures, opaque beneficial ownership arrangements, or links to high-risk industries. Applying a risk-based approach helps organisations prioritise customer due diligence (CDD) and enhanced due diligence (EDD) measures where they are needed most.

Evaluating Geographic and Jurisdictional Risk

Geographic risk is a critical component of UK AML compliance. Businesses should assess whether customers, counterparties, or transactions are connected to high-risk countries, sanctioned jurisdictions, or regions known for corruption, terrorist financing, or weak AML controls. Sanctions screening, adverse media checks, and ongoing monitoring can help identify emerging risks associated with specific jurisdictions. Understanding geographic exposure enables firms to strengthen AML controls and make informed compliance decisions.

Understanding Product and Service Risk Exposure

Different products and services present varying levels of financial crime risk. Services that facilitate rapid movement of funds, cross-border transactions, anonymous payments, or complex investment structures may attract greater scrutiny from regulators. Financial institutions and regulated businesses should evaluate how their products could potentially be misused for money laundering and implement appropriate AML screening, transaction monitoring, and risk management controls to mitigate exposure.

Identifying Transaction-Based Risks

Transaction risk focuses on the nature, frequency, size, and pattern of customer activity. Unusually large transfers, inconsistent transaction behaviour, frequent international payments, or activity that does not align with a customer's known profile may indicate potential money laundering concerns. Effective transaction monitoring systems help businesses detect suspicious activity, generate alerts, and support timely Suspicious Activity Report (SAR) submissions when necessary.

Analysing Delivery Channel and Onboarding Risks

The way customers are onboarded can affect AML risk levels. Non-face-to-face onboarding, digital account opening, third-party introductions, and remote verification may increase the risk of identity fraud or impersonation if not properly managed. Strong KYC procedures, biometric verification, and secure onboarding controls help organisations maintain compliance while delivering a smooth customer experience.

By assessing customer, geographic, product, transaction, and delivery channel risks together, businesses can build a stronger AML compliance framework. A well-structured AML risk assessment supports accurate risk scoring, effective resource allocation, stronger financial crime prevention, and compliance with UK regulatory expectations.

AML Compliance Best Practices

Implementing AML compliance best practices helps UK businesses reduce financial crime risks, meet regulatory obligations, and strengthen their overall compliance framework.

By adopting a risk-based approach, enhancing customer due diligence, automating AML screening, and maintaining effective ongoing monitoring, organisations can build a more resilient and efficient AML compliance programme.

Adopt a Risk-Based Approach

A risk-based approach is the foundation of effective AML compliance in the UK. Rather than applying the same level of scrutiny to every customer, businesses should assess customer risk, geographic exposure, transaction patterns, products, and delivery channels to determine where financial crime threats are most likely to arise. This enables organisations to allocate compliance resources efficiently while meeting UK AML regulations and customer due diligence requirements.

By implementing robust AML risk assessments, businesses can identify high-risk customers, trigger enhanced due diligence (EDD) where necessary, and strengthen ongoing monitoring processes. A well-designed risk-based framework helps reduce exposure to money laundering, terrorist financing, sanctions breaches, and fraud while supporting regulatory expectations from the FCA, HMRC, and other supervisory authorities.

Automate Screening and Monitoring

Manual AML checks can be slow, inconsistent, and difficult to scale. Automating AML screening, sanctions screening, PEP screening, and adverse media checks allows businesses to identify risks faster and maintain continuous compliance throughout the customer lifecycle. Automated systems can also reduce false positives and improve operational efficiency.

Continuous AML monitoring ensures that changes in customer risk profiles, sanctions lists, beneficial ownership structures, or negative news are detected in real time. Modern AML compliance software helps organisations stay compliant by providing alerts, risk scoring, audit trails, and ongoing due diligence capabilities that support a proactive compliance programme.

Maintain Clear Audit Trails

Comprehensive audit trails are essential for demonstrating AML compliance and satisfying regulatory inspections. Businesses should maintain accurate records of customer onboarding, identity verification, risk assessments, screening results, enhanced due diligence activities, and suspicious activity investigations.

Clear documentation creates transparency and enables compliance teams to evidence decision-making processes when reviewed by regulators or auditors. Strong record-keeping practices also support internal governance, reduce compliance gaps, and help organisations respond quickly to regulatory requests or investigations.

Train Employees Regularly

Employees play a critical role in detecting suspicious activity and preventing financial crime. Regular AML training ensures staff understand money laundering risks, customer due diligence obligations, sanctions requirements, and internal reporting procedures. Training should be tailored to specific roles and updated to reflect regulatory changes.

A well-informed workforce is more likely to identify red flags, escalate concerns appropriately, and contribute to a strong compliance culture. Ongoing education helps businesses reduce human error, improve risk awareness, and strengthen their overall AML compliance framework.

Review AML Controls Frequently

AML risks evolve constantly as criminals adopt new methods and regulations continue to change. Businesses should regularly review their AML policies, procedures, risk assessments, and monitoring controls to ensure they remain effective and aligned with current regulatory expectations.

Periodic reviews help identify weaknesses, improve operational efficiency, and ensure compliance programmes adapt to emerging threats. Frequent testing and refinement of AML controls can significantly reduce exposure to regulatory penalties and financial crime risks.

Conduct Independent Testing

Independent testing provides an objective assessment of whether an AML compliance programme is functioning as intended. Reviews may be conducted by internal audit teams, external consultants, or specialist compliance professionals who evaluate policies, controls, screening processes, and reporting procedures.

Regular independent assessments help uncover gaps that may not be visible during day-to-day operations. They also demonstrate a commitment to continuous improvement, strengthen governance, and provide valuable assurance that AML controls are effective, proportionate, and compliant with UK AML requirements.

Try Free AML Screening Tools with Binderr

Common AML Compliance Challenges

UK AML compliance presents a range of operational, regulatory, and technological challenges for regulated businesses.

From customer due diligence and AML screening to ongoing monitoring and risk management, organisations must balance compliance obligations with efficiency, accuracy, and customer experience.

False Positives - False positives are one of the most common AML compliance challenges. Sanctions screening, PEP screening, and adverse media checks can generate alerts that match legitimate customers, requiring additional review and investigation. High volumes of false positives can increase operational costs, slow onboarding, and place pressure on compliance teams.

One of the biggest AML compliance challenges is managing false positives. Compliance teams must review alerts, validate matches, document decisions, and maintain a clear audit trail that can be presented during regulatory reviews or audits.

(Binderr centralises PEP, sanctions, and media matches into a structured review queue so analysts can investigate risks faster.)

Complex Ownership Structures - Identifying beneficial ownership can be difficult when businesses operate through multiple entities, trusts, holding companies, or international corporate structures. AML regulations require firms to verify ultimate beneficial owners (UBOs), but tracing ownership and control across several jurisdictions can be time-consuming and resource-intensive.

Cross-Border Compliance - Businesses operating internationally must navigate different AML regulations, sanctions regimes, and customer due diligence requirements across multiple jurisdictions. Maintaining consistent AML controls while meeting local regulatory obligations can be challenging, particularly for financial institutions, fintechs, and global service providers.

Regulatory Changes - AML regulations continue to evolve in response to emerging financial crime risks, technological developments, and geopolitical events. Organisations must regularly review and update their AML compliance programmes, policies, and procedures to ensure they remain aligned with current UK AML requirements and regulatory expectations.

Resource Constraints - Many organisations face limitations in staffing, budget, and compliance expertise. Manual AML checks, ongoing monitoring, and risk assessments can consume significant resources, making it difficult for teams to manage growing compliance workloads efficiently without automation and scalable processes.

Customer Experience vs Compliance - Businesses must balance strong AML controls with a smooth customer onboarding experience. Lengthy verification processes, repeated document requests, and manual reviews can create friction for customers. Effective AML compliance solutions help organisations meet regulatory requirements while reducing onboarding delays and improving customer satisfaction.

AML Screening, Monitoring & Risk Assessment in One Platform

AML compliance depends on more than sanctions screening alone. Businesses need a complete view of customer risk across onboarding and ongoing monitoring.

- Screen individuals and businesses against sanctions lists, watchlists, and PEP databases

- AI-powered adverse media screening across global sources

- Smart matching technology to reduce false positives

- Continuous monitoring with real-time alerts

- Dynamic risk scoring for CDD and EDD decisions

- Support for trusts, foundations, partnerships, vessels, and complex entities

- Integrated KYC and KYB verification workflows

Bottom Line

AML compliance is essential for UK businesses operating in regulated sectors. A strong compliance framework should include risk assessments, customer due diligence, sanctions and PEP screening, beneficial ownership verification, suspicious activity reporting, and ongoing monitoring.

By adopting a risk-based approach and leveraging AML automation, organisations can improve efficiency, reduce compliance risks, and maintain regulatory confidence. Effective AML compliance not only helps meet legal obligations but also supports stronger risk management, customer trust, and long-term business growth.

For organisations looking to simplify AML compliance, Binderr Compliance provides an all-in-one platform for KYC, KYB, AML screening, sanctions checks, ongoing monitoring, and automated risk management.