As one of the world's leading international finance centres, Jersey is trusted by banks, investment firms, trust companies, fund administrators, and corporate service providers across global markets. Its strong regulatory framework and commitment to financial crime prevention, money laundering prevention, and regulatory compliance have helped establish Jersey as a respected jurisdiction for cross-border financial services.

Beyond being a regulatory requirement, AML compliance serves as a key safeguard against money laundering, terrorist financing, proliferation financing, sanctions evasion, fraud, and corruption. According to the United Nations Office on Drugs and Crime (UNODC), an estimated 2% to 5% of global GDP is laundered each year, highlighting the scale of financial crime risks facing businesses worldwide.

This guide explains the core elements of an effective AML framework, including Know Your Customer (KYC), Know Your Business (KYB), customer due diligence, enhanced due diligence, AML screening, sanctions screening, PEP screening, adverse media screening, beneficial ownership verification, UBO verification, transaction monitoring, ongoing monitoring, and suspicious activity reporting. By following these best practices, businesses can meet regulatory expectations, reduce risk, and create a more efficient compliance process.

Binderr AML Screening Solution

- Global sanctions, watchlist, and PEP screening

- Adverse media screening across thousands of sources

- Continuous monitoring and real-time alerts

- Risk-based scoring for CDD and EDD

- Business and individual screening capabilities

- Smart matching technology to reduce false positives

- Audit trails and compliance reporting

What Is AML Compliance?

AML compliance refers to the policies, procedures, and controls that businesses use to prevent, detect, and report money laundering, terrorist financing, proliferation financing, and other forms of financial crime. Anti-money laundering (AML) regulations are designed to protect the integrity of the financial system by ensuring that organisations understand who their customers are, assess risk appropriately through customer risk assessments, and identify suspicious activity before it causes harm. In Jersey, AML compliance is a core regulatory expectation for many regulated businesses and forms a critical part of broader financial crime prevention programmes.

AML Compliance Framework

AML Compliance

│

├── KYC (Identity Verification)

├── KYB (Business Verification)

├── CDD (Standard Due Diligence)

├── EDD (Enhanced Due Diligence)

├── AML Screening

│ ├── Sanctions Screening

│ ├── PEP Screening

│ └── Adverse Media Checks

└── Ongoing Monitoring

├── Risk Reviews

├── Ownership Changes

└── Suspicious Activity Detection

This framework illustrates how AML compliance combines customer verification, beneficial ownership verification, customer risk assessment, screening, due diligence, transaction monitoring, record keeping, and continuous monitoring to create a comprehensive defence against financial crime.

Access Free Binderr Screening Tool

Why AML Compliance Matters in Jersey

AML compliance is essential for protecting Jersey’s financial system from money laundering, terrorist financing, proliferation financing, sanctions breaches, and other forms of financial crime.

As a leading international finance centre, Jersey businesses must meet strict AML regulations, implement robust KYC and customer due diligence processes, conduct beneficial ownership verification, and maintain effective ongoing monitoring and transaction monitoring to satisfy regulatory expectations and manage risk.

Prevents money laundering and financial crime - AML screening, adverse media screening, and transaction monitoring help identify suspicious activity, sanctioned individuals, politically exposed persons, and potential financial crime risks before they impact your business. Effective controls support the detection and prevention of money laundering throughout the customer lifecycle.

Meets JFSC regulatory requirements - AML screening supports compliance with Jersey Financial Services Commission (JFSC) requirements by helping businesses carry out appropriate customer checks, customer risk assessments, sanctions screening, and ongoing monitoring. This helps demonstrate a strong commitment to regulatory compliance.

Reduces compliance and reputational risk - By identifying high-risk customers and transactions early, AML screening helps reduce the likelihood of regulatory breaches, financial penalties, and reputational damage. Strong compliance processes, audit trails, and risk-based controls can also improve stakeholder confidence.

Strengthens customer due diligence controls - AML screening enhances customer due diligence (CDD) by verifying customer information against relevant watchlists, sanctions lists, PEP databases, and risk databases. This supports more informed risk assessments, customer onboarding decisions, and financial crime prevention efforts.

Protects Jersey's financial system integrity - Robust AML screening contributes to the integrity and stability of Jersey’s financial system by helping prevent illicit funds from entering regulated businesses. This supports a safer and more trusted financial environment while strengthening anti-money laundering controls.

Streamline AML Compliance Workflows with Binderr

- Run KYC, KYB, and AML checks from a single platform

- Verify individuals using AI-powered identity verification

- Verify businesses through global company registries

- Identify and verify Ultimate Beneficial Owners (UBOs)

- Generate dynamic customer risk scores automatically

- Collect additional documents through configurable workflows

- Maintain complete audit trails and compliance records

Jersey AML Regulatory Framework

Understand the key regulations and obligations that shape anti-money laundering compliance in Jersey.

Explore the AML regulatory framework, JFSC requirements, customer due diligence (CDD), risk-based approaches, beneficial ownership verification obligations, and financial crime prevention measures.

Key AML Legislation

Proceeds of Crime (Jersey) Law

The Proceeds of Crime (Jersey) Law is the cornerstone of Jersey’s anti-money laundering framework. Its primary purpose is to prevent criminals from benefiting from the proceeds of unlawful activities by criminalising money laundering and establishing mechanisms for the identification, reporting, restraint, and confiscation of criminal assets. The law applies to a wide range of financial institutions and designated non-financial businesses and professions (DNFBPs), requiring them to implement robust AML controls, suspicious activity reporting procedures, customer due diligence measures, and effective record-keeping practices.

Money Laundering (Jersey) Order

The Money Laundering (Jersey) Order sets out the practical AML and counter-financing of terrorism (CFT) obligations that regulated businesses must follow. Key requirements include customer due diligence (CDD), enhanced due diligence (EDD) for higher-risk customers, ongoing monitoring of business relationships, record-keeping, customer risk assessment, beneficial ownership verification, employee training, and transaction monitoring. The Order plays a critical role in ensuring that firms adopt a risk-based approach to AML compliance and financial crime prevention.

Terrorism (Jersey) Law

The Terrorism (Jersey) Law establishes legal obligations aimed at preventing terrorist financing and supporting national and international security efforts. It criminalises the raising, possession, use, or movement of funds intended for terrorist purposes and requires businesses to identify and report suspicious transactions linked to terrorism through suspicious activity reporting mechanisms. Compliance with this legislation is essential for detecting and disrupting terrorist financing networks.

Sanctions and Asset-Freezing Laws

Jersey’s sanctions and asset-freezing regime requires businesses to comply with applicable financial sanctions, trade restrictions, and asset-freezing measures. Firms must screen customers, beneficial owners, transactions, and counterparties against relevant sanctions lists and take immediate action when a match is identified. Effective sanctions compliance, sanctions screening, and ongoing monitoring help prevent dealings with sanctioned individuals, entities, and jurisdictions while supporting global efforts to combat financial crime and geopolitical threats.

AML/CFT/CPF Handbook

The AML/CFT/CPF Handbook issued by the Jersey Financial Services Commission (JFSC) provides detailed guidance on meeting regulatory obligations relating to anti-money laundering, countering the financing of terrorism, and countering proliferation financing. The Handbook outlines regulatory expectations, best practices, risk-based compliance measures, governance requirements, customer due diligence standards, source of funds checks, source of wealth verification, and beneficial ownership verification requirements. It serves as an essential reference for regulated businesses seeking to maintain effective compliance programmes and demonstrate adherence to Jersey’s regulatory framework.

International Standards

- FATF Recommendations: The Financial Action Task Force (FATF) Recommendations form the global benchmark for AML, CFT, and proliferation financing controls. Jersey aligns its regulatory framework with these internationally recognised standards to maintain a strong and effective compliance environment.

- OECD standards: OECD initiatives promote transparency, tax compliance, beneficial ownership disclosure, UBO verification, and international cooperation. Businesses operating in Jersey must understand how these standards influence governance, reporting, and regulatory expectations.

- International sanctions frameworks: Global sanctions regimes, including those implemented by the United Nations, United Kingdom, European Union, and other authorities, require firms to maintain effective sanctions screening, adverse media screening, and monitoring processes.

- Cross-border compliance expectations: Financial institutions operating internationally must manage varying regulatory requirements across jurisdictions, conduct enhanced due diligence on cross-border relationships, verify source of funds and the source of wealth where appropriate, and maintain strong AML governance to address evolving financial crime risks and regulatory scrutiny.

Get Free AML Insights Instantly with Binderr

The Core Components of an AML Compliance Programme

An effective AML compliance programme is built on a framework of policies, controls, and monitoring processes designed to prevent financial crime.

Key areas include risk assessment, customer due diligence (CDD), ongoing monitoring, transaction monitoring, employee training, internal controls, compliance automation, and regulatory reporting.

Risk Assessment and Customer Risk Profiling

Risk assessment and customer risk profiling form the foundation of an effective Anti-Money Laundering (AML) framework. Financial institutions evaluate customers based on factors such as geographic location, source of funds, source of wealth, transaction behaviour, industry sector, and ownership structure.

By assigning risk ratings through a customer risk assessment process, organisations can apply appropriate controls, allocate compliance resources efficiently, and identify potential money laundering, terrorist financing, proliferation financing, and financial crime risks.

Know Your Customer (KYC)

Know Your Customer (KYC) procedures help organisations verify the identity of individuals before establishing a business relationship. This process typically includes collecting identification documents, verifying personal information, conducting identity verification, and understanding the customer's financial activities. Effective KYC controls support regulatory compliance, fraud prevention, customer onboarding, and risk management.

Know Your Business (KYB)

Know Your Business (KYB) focuses on verifying corporate entities and understanding their ownership and operational structure. This includes validating company registration details, identifying directors, reviewing business activities, conducting beneficial ownership verification, and determining Ultimate Beneficial Owners (UBOs). Robust KYB processes and UBO verification help prevent the misuse of corporate structures for money laundering, sanctions evasion, and other illicit activities.

AML and Sanctions Screening

AML and sanctions screening involves checking customers, businesses, beneficial owners, and transactions against global sanctions lists, watchlists, politically exposed persons (PEP) databases, and adverse media sources. Continuous screening, adverse media screening, and sanctions monitoring help organisations detect high-risk relationships, comply with international regulations, and mitigate exposure to financial crime and regulatory penalties.

Modern AML screening platforms allow compliance teams to screen individuals and businesses against sanctions lists, PEP databases, watchlists, and adverse media sources within seconds. The process typically begins by entering customer information and running an automated risk assessment against global data sources.

(Example of an AML screening workflow in Binderr, allowing compliance teams to screen individuals and organisations against sanctions, PEPs, watchlists, and adverse media databases.)

Customer Due Diligence (CDD)

Customer Due Diligence (CDD) is the process of gathering and assessing information about customers to understand who they are, the nature of their activities, and the purpose of the business relationship. CDD measures enable organisations to identify risks early, verify customer legitimacy, conduct customer risk assessments, and maintain compliance with AML regulations and industry standards.

Enhanced Due Diligence (EDD)

Enhanced Due Diligence (EDD) applies additional scrutiny to higher-risk customers, transactions, or jurisdictions. This may include obtaining detailed source of wealth and source of funds information, conducting deeper background checks, enhanced adverse media screening, and increasing monitoring frequency. EDD strengthens risk mitigation efforts and helps organisations manage complex compliance obligations.

Ongoing Monitoring and Reviews

Ongoing monitoring ensures that customer profiles remain accurate and that transactions continue to align with expected behaviour. Regular reviews, transaction monitoring systems, sanctions screening updates, and risk reassessments help identify unusual activity, emerging risks, ownership changes, and changes in customer circumstances. Continuous monitoring is a critical component of an effective AML compliance programme.

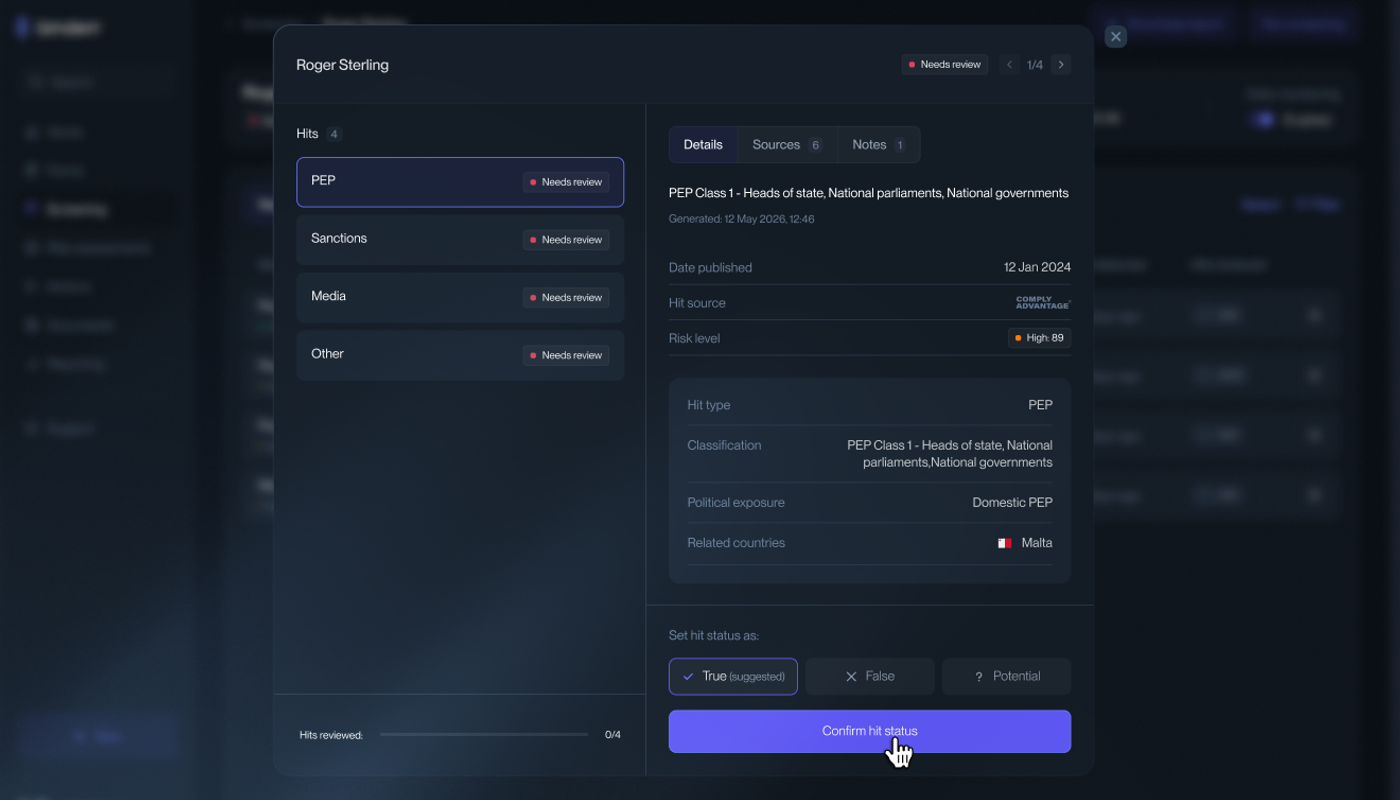

Once a potential match is identified, compliance teams must review supporting information, evaluate risk levels, assess source data, and determine whether the result is a true match, false positive, or potential match requiring further investigation.

(Binderr provides detailed screening investigation workflows, allowing compliance teams to review sanctions, PEP, and adverse media matches before making risk decisions.)

Suspicious Activity Reporting (SAR)

Suspicious Activity Reporting (SAR) requires organisations to identify, investigate, and report potentially suspicious transactions or behaviours to the relevant authorities. Timely and accurate suspicious activity reports support law enforcement efforts, demonstrate regulatory compliance, and contribute to the detection and prevention of financial crime.

Record Keeping and Documentation

Maintaining comprehensive records and documentation is essential for demonstrating compliance with AML regulations. Organisations must retain customer identification records, transaction histories, risk assessments, screening results, due diligence documentation, audit trails, and beneficial ownership verification records for prescribed periods. Effective record keeping supports audits, regulatory inspections, and internal investigations.

AML Governance and Oversight

AML governance and oversight provide the strategic framework for managing compliance risks across an organisation. This includes establishing policies and procedures, assigning accountability to senior management, conducting staff training, performing independent audits, maintaining audit trails, and ensuring regulatory reporting obligations are met. Strong governance promotes a culture of compliance, enhances operational resilience, and protects the integrity of the financial system.

Common AML Compliance Mistakes Jersey Businesses Make

Understanding common AML compliance mistakes can help Jersey businesses strengthen their regulatory processes and avoid costly penalties.

Key areas include customer due diligence (CDD), ongoing monitoring, AML regulations, customer risk assessments, record keeping, beneficial ownership verification, and financial crime prevention.

Inadequate customer verification - Weak customer verification can lead to gaps in Know Your Customer (KYC) procedures, making it difficult to confirm a customer's identity and assess potential risks. This increases exposure to fraud, money laundering, terrorist financing, and regulatory breaches.

Failure to identify UBOs - Failing to identify Ultimate Beneficial Owners (UBOs) can obscure who ultimately controls or benefits from a business relationship. This creates compliance risks and may prevent firms from meeting anti-money laundering (AML) requirements, beneficial ownership verification obligations, and transparency standards.

Weak sanctions screening - Ineffective sanctions screening can result in transactions involving sanctioned individuals, entities, or jurisdictions going undetected. This can lead to regulatory penalties, financial losses, reputational damage, and failures in financial crime prevention controls.

Poor documentation - Incomplete or inaccurate documentation makes it difficult to demonstrate compliance with regulatory obligations. It can also create challenges during audits, investigations, customer due diligence reviews, and regulatory inspections.

Lack of ongoing monitoring - Without ongoing monitoring and transaction monitoring, changes in customer behaviour, risk profiles, ownership structures, or transaction patterns may go unnoticed. Continuous monitoring helps identify suspicious activity and supports effective AML compliance.

Outdated risk assessments - Risk assessments that are not regularly reviewed may fail to reflect current threats, regulatory changes, emerging financial crime risks, or business activities. Keeping assessments up to date helps ensure appropriate controls remain in place.

Manual compliance processes - Reliance on manual compliance processes can increase the likelihood of human error, inconsistencies, and delays. Compliance automation and RegTech solutions can improve efficiency, accuracy, audit trail management, and regulatory reporting capabilities.

Real-Time AML Screening and Ongoing Monitoring with Binderr

AML compliance does not stop after onboarding. Customer risk profiles can change at any time due to new sanctions, adverse media exposure, political appointments, ownership changes, or emerging financial crime concerns.

- Detect new sanctions matches automatically

- Monitor PEP status changes

- Track adverse media developments

- Identify ownership and UBO changes

- Support ongoing customer risk assessments

- Strengthen transaction and behavioural monitoring

AML Compliance Checklist for Jersey Businesses

Ensure your business meets Jersey's anti-money laundering requirements with a clear and practical compliance framework.

Key areas include AML compliance, customer due diligence (CDD), Know Your Customer (KYC), Know Your Business (KYB), risk assessments, ongoing monitoring, transaction monitoring, record keeping, and regulatory reporting.

- AML policy established - An AML policy has been established to define the organisation’s approach to anti-money laundering compliance. It outlines responsibilities, controls, procedures, and governance measures for identifying and managing financial crime risks.

- Risk assessment completed - A comprehensive risk assessment has been completed to identify and evaluate money laundering, terrorist financing, and proliferation financing risks. The findings help determine the appropriate level of controls and monitoring required.

- KYC procedures implemented - Know Your Customer (KYC) procedures have been implemented to verify customer identities and assess risk profiles. These procedures support regulatory compliance, identity verification, and help prevent fraudulent activity.

- KYB verification procedures implemented - Know Your Business (KYB) verification procedures have been implemented to validate business entities and confirm their legitimacy. This includes reviewing company information, ownership structures, beneficial ownership verification requirements, and relevant documentation.

- UBO verification process established - A process has been established to identify and verify Ultimate Beneficial Owners (UBOs). This helps ensure transparency of ownership, supports UBO verification requirements, and strengthens compliance with AML regulations.

- AML screening conducted - AML screening is conducted against relevant sanctions lists, watchlists, politically exposed persons (PEP) databases, and adverse media screening sources. Screening helps identify potential risks before and during the customer relationship.

- CDD and EDD procedures documented - Customer Due Diligence (CDD) and Enhanced Due Diligence (EDD) procedures have been documented to support risk-based compliance measures. These procedures outline the steps required for standard and higher-risk customers, including source of funds and source of wealth checks where necessary.

- Ongoing monitoring enabled - Ongoing monitoring and transaction monitoring have been enabled to review customer activity and identify unusual or suspicious transactions. This supports continuous compliance and risk management throughout the customer lifecycle.

- SAR procedures established - Suspicious Activity Report (SAR) procedures have been established to ensure potential financial crime concerns are identified, escalated, and reported appropriately. Clear suspicious activity reporting processes support regulatory obligations.

- Staff training completed - Staff have completed AML and compliance training to ensure they understand their responsibilities and can recognise potential indicators of financial crime. Regular training helps maintain awareness of regulatory requirements, sanctions obligations, and AML best practices.

- Audit trails maintained - Audit trails are maintained to provide a clear record of compliance activities, decisions, customer interactions, and due diligence actions. These records support accountability, transparency, and regulatory reviews.

Get a Complete AML Compliance Solution with Binderr

- Detect new sanctions matches automatically

- Monitor PEP status changes

- Track adverse media developments

- Identify ownership and UBO changes

- Support ongoing customer risk assessments

- Strengthen transaction and behavioural monitoring

- Reduce manual compliance reviews

Bottom Line

AML compliance is a key requirement for regulated businesses in Jersey. It helps protect organisations from financial crime, fraud, and money laundering risks. A strong AML framework includes KYC, KYB, sanctions screening, risk assessments, customer due diligence (CDD), enhanced due diligence (EDD), and ongoing monitoring. Together, these measures support regulatory compliance and effective risk management.

Modern AML technology helps streamline compliance processes and automate verification checks. It also improves accuracy, reduces manual effort, and supports faster customer onboarding. By investing in effective AML solutions, businesses can better manage risk, meet JFSC expectations, build customer trust, and grow with confidence.

Discover trusted compliance solutions and business services on Binderr Compliance to simplify your AML and regulatory requirements.